29th April 2026

Key takeaways

- In a fast-changing financial landscape there is no single ‘almost ideal’ stress test: the best way-forward to identify and assess the risks for financial stability is to develop a range of complementary analytical tools.

- This policy-brief advocates the development of a comprehensive range of analytical tools ― each one with very specific objectives but providing complementary perspectives ― to assess the most fundamental risks for the preservation of financial stability.

- The system wide stress test ― including banks, investment funds, pension funds and insurers ― focus on capital adequacy, as it assesses how capital ratios would behave in an environment of persistently higher risk premiums and stress in the financial sector, allowing for contagion between banks and non-banks.

- The reverse stress test, which is an exploratory exercise conducted as part of the ICAAP, exposes idiosyncratic vulnerabilities at the individual level ― that would very likely remain undetected under a common adverse scenario ― and therefore is very insightful for the micro supervisor.

- A sensitivity analysis on profitability provides an assessment of the sustainability of the business model at the individual level, assessing how individual institutions intend to respond to the key trends in finance (digitalization, new financial players, artificial intelligence, outsourcing, cyber insecurity).

Why the use of stress testing needs to be enhanced

Stress testing played a prominent role in the capitalization of banking sectors since the Global Financial Crisis (GFC). A recent BCBS working paper (BCBS, 2025) identifies the main benefits of micro-supervisory stress tests over the last 20 years: (i) they lower risk levels for banks, particularly when a strong supervisory scrutiny is exerted during the exercise, (ii) they increase market discipline and improve financial stability through public disclosure of results, and (iii) they proved to be particularly successful as a crisis management tool to rebuild trust in the banking sector in turbulent times. There are no doubts about that: stress testing contributed decisively to strengthen the resilience of the banking sector and, as a result, of the financial system.

It is also true that there are very good reasons to give a further impulse on the use of stress testing. As the editors of this Forum have expressed in the opening statement “in a moment in which ― after gaining a compelling relevance during the GFC and, since then, playing a prominent role in the assessment of capital levels in the banking sector ― the benefits of repeating the current stress testing exercises seem to be declining”. A series of policy contributions for the Forum ― (Schuermann, 2026), (de la Mora, 2026), (Valderrama, 2026), (Aikman, 2026) ― discuss how stress testing could be strengthened in future exercises.

There are five main reasons to redesign the use of stress testing.

1. The possibilities to develop more severe adverse scenarios than the ones already considered have largely been exhausted. Recent ECB research (ECB, 2025) shows that the adverse scenarios in the EU-wide stress tests reached the highest levels of severity in the last two exercises (2023 and 2025). Increasing the severity of repetitive adverse scenarios does not bring any visible contribution, particularly when capital flexibility (de la Mora, 2026) is high due to ample capital buffers (ECB-FSR, November 2025).

2. Considering a single adverse scenario has proved to be insufficient to capture the full spectrum of idiosyncratic risks relevant at the level of individual institutions, which differ markedly in terms of business model, complexity, risk profiles and geographic dimension. This aspect is even more important in the current context of exceptionally high uncertainty, as the characteristics of adverse shocks may assume many different forms. A shift favoring the exploratory and diagnostic characteristics of stress testing is therefore needed (Aikman, 2026).

3. The supervisory process has not been completely successful in exploring the results of bank specific stress testing (ICAAP). Under full banks’ ownership and thorough scrutiny by supervisors, ICAAP exercises ― also when designed as reverse stress testing ― are particularly useful as an exploratory instrument aiming the identification of the most relevant idiosyncratic vulnerabilities. Moreover, they also constitute a useful tool for risk management and crisis prevention.

4. The landscape of the global financial system is changing rapidly, and two predominant features are worth highlighting (De Cos, 2025): the all-time highs in public debt in many geographies and the fast expansion of the non-banking sector. These two major changes interact as there is a fast-rising participation of non-banking financial institutions in sovereign bond markets. In addition, the increasing role of non-banks in corporate credit intermediation brings new financial stability risks (IMF, 2025). This makes the case for an enhanced use of system-wide stress tests accounting for the interconnections between the segments of the financial sector (ECB/ESRB, 2026).

5. Finally, many recent trends in finance ― digitalization, new financial players, artificial intelligence, outsourcing, cyber insecurity ― raise important issues for the future profitability of the banking sector. Will banks manage to achieve sustainable levels of profitability in such a challenging and fast-changing environment?

How should stress testing adjust…

The very broad nature of the five aspects discussed above tends to exclude the possibility of having an ‘almost ideal’ stress test that could address all of them. This policy-brief advocates the development of a range of comprehensive analytical tools ― each one with very specific objectives but providing complementary perspectives ― to assess the most fundamental risks for the preservation of financial stability. This discussion has a predominant euro area lens, but all the suggestions would also apply for other geographies.

What should then be the priorities?

… system-wide stress testing…

Linkages between banks and the non-bank financial intermediation sector have increased significantly and need to be better understood from a financial stability perspective, particularly having in mind the leverage and liquidity vulnerabilities in some segments of the non-banking sector that have been identified by many international organizations (FSB, IMF, ECB). Interconnectedness between the banking and non-banking sectors exists from many channels (ECB/ESRB, 2026). A granular and forward-looking cross-sectoral perspective is fundamental to identifying the main threats to financial stability.

This recommends a system-wide approach including banks, investment funds, pension funds and insurers. System-wide stress testing accounts for interactions (e.g. contagion and amplifications) across the different segments of the financial sector and are well designed to capture the transmission of shocks across the financial sector.

The Bank of England sow the seeds for system-wide stress testing. The results of the first system-wide exploratory scenario (SWES) were published in November 2024 (BofE, 2024). Last October, the Bank of England announced a second system-wide exercise ― focused on the private markets ecosystem ― aiming a better understanding of how interactions between banks and non-bank financial institutions could amplify stress across the financial system. The ECB has developed a very comprehensive work on macro stress testing, firstly through the BEAST (ECB, 2023) and, more recently, with the 2025 Macroprudential Stress Test Extension report (ECB, 2025), which included a system-wide analysis with amplification effects between banks and non-banks. Also, in 2025, the IMF presented a system-wide stress testing, as part of the FSAP for the euro area, with a specific focus on non-banking financial institutions (IMF, 2025). Finally, the Banque de France, the ACPR and the AMF announced a first system-wide stress test for the French financial system (AMF, 2025).

What should be the key features of a system-wide stress test for the euro area? As said, all types of financial institutions ― banks, investment funds, pension funds and insurers ― should be included and the interactions (contagion, amplification, spillovers) between the different segments of the financial sector should be explicitly modelled. Non-banks are a very diverse and heterogeneous set of financial institutions (Buenaventura, 2025), entailing a variety of different risks, some of them much more concerning than the others. (De Cos, 2025) identifies a set of potential financial stress amplification channels, possibly inducing non-linear yield spikes, reflecting the increasing role of NBFIs in the intermediation of public debt.

A recent ECB blog (ECB, 2026) shows that the European investment fund sector is highly concentrated, as the largest 15 asset management groups account for about half the total assets of euro area funds. It would be advisable to incorporate them in the stress test. This system-wide exercise requires closing some informational gaps that have been identified by the BIS and the FSB, amongst others (Buenaventura, 2025).

The above-mentioned exercises of the Bank of England and the IMF, as well as some ECB exercises (ECB, 2025b), considered short-term horizons to explore contagion effects under the adverse scenario. (IMF, 2025), for instance, develops a system-wide liquidity stress test focused on the very short-term, as the two market scenarios corresponded to time horizons of two days and two weeks.

The policy brief suggests focusing more on capital and much less in liquidity, as it recommends assessing the risks for financial stability if higher risk premiums in both corporate and sovereign yields persist in longer horizons. This favors the usual two-three-year horizon. One important feature should be the assessment of how large and more leveraged corporates could cope with difficulties in refinancing and repaying the existing debt in such a prolonged adverse scenario (in a context of downgrades and rising costs of debt).

This exercise has a different (but complementary) nature of the system-wide exercises that have predominantly focused on the short term (as they were inspired by episodes like the March 2020 dash-for-cash, the commodity shock in late 2021-2022 following Russia's invasion of Ukraine, the UK gilts episode in 2022, and the March 2023 banking turmoil). Instead, defining a two-three-year horizon captures a longer adverse period ― with persistent stress on corporate and public bonds ― more similar to the 2011-2013 crisis in the euro area.

This exercise should be run predominantly from a top-down perspective, possibly leveraging on the previous use of system-wide stress testing for the euro area, to understand the interplay between the banking sector and the real economy, the different segments of the financial sector, and accounting for the interactions with large leveraged corporates.

… reverse stress testing…

The current stress tests restrict attention to a single adverse scenario. However, a specific bank may perform very well under a specific adverse scenario and, nonetheless, be severely affected in alternative, and as plausible, scenarios that may expose much more directly its vulnerabilities. There are two ways to overcome this drawback: to consider multiple adverse scenarios or to take advantage of reverse stress testing. This second route seems to be a more promising one.

Reverse stress testing answers the question “which combination of events could lead to specific consequences for the institution” (for instance the depletion of solvency levels by x percentage points), whereas stress testing answers the question “if these events occur, what would be the consequences for the institution” (again in terms of depletion of capital ratios).

Reverse stress testing brings additional perspectives vis-à-vis traditional stress tests: captures severe idiosyncratic events that are not easily covered in a common adverse scenario; identifies hidden banks’ vulnerabilities that otherwise could remain undetected for the supervisor; makes ICAAP much more focused by setting a metric for capital depletion; clarifies how banks are prepared to react and to improve their recovery plans.

The ICAAP plays a key role in risk management and capital planning of credit institutions. Under the current regulatory framework, institutions are supposed to develop ICAAP baseline projections and ICAAP stressed projections. These last ones correspond to the identification of institution-specific adverse scenarios, reflecting idiosyncratic vulnerabilities of the institution. The industry has been claiming that ICAAP is not adequately integrated in the supervisory process.

The ECB announced in December 2025 (ECB, 2025c) that a reverse stress test will be launched to capture the possible effects of geopolitical risks. Banks will be asked to identify the relevant geopolitical events that could produce a depletion of (at least) 300-basis point in CET1. The ECB has also stated that this exercise ― which will be conducted as part of the ICAAP ― aims to foster bank’s own risk management and to improve their capacity to develop prudent capital and recovery plans.

Geopolitical risks have a very broad nature: armed conflicts, regional instability, supply side disruptions, trade barriers, economic sanctions, and cybersecurity threats. The reverse stress test will bring extremely useful information for the banks and for the supervisor. A recent joint ESRB/ECB report (ECB/ESRB, 2026) documents how geoeconomic fragmentation creates sizeable financial stability risks.

The last ECB’s Financial Stability Review (ECB-FSR, November 2025) has identified the most evident vulnerabilities in the financial sector: high asset valuations, a challenging fiscal outlook in several advanced economies, credit risk exposures to sectors sensitive to trade frictions. All these vulnerabilities are amplified by the linkages between banks and non-banks. Geopolitics is just one of the possible sources of risk that could challenge the preservation of financial stability.

An effective reverse stress test requires the design of scenarios sufficiently adverse ― idiosyncratically adverse ― to contribute to the identification and understanding of the most salient weaknesses of a bank. Under adequate supervisory scrutiny, this improves knowledge about the bank’s own most salient vulnerabilities. The benefits from the use of reverse stress testing will the higher the broader the nature of the source of risks that could lead to the envisaged capital depletion.

… forward-looking sensitivity analysis on banking profitability…

Whereas most of the banking sector has achieved prudent capital and liquidity positions, it is the case that a sizeable proportion of the sector displays modest profitability ratios. As a complement to focusing mainly on solvency and liquidity metrics, it is important to assess the prospects to preserve (or to achieve) sustainable levels of profitability:

- Will banks manage to close the gap between return and cost on equity through credible cost reduction measures, efficiency gains, income diversification and other business model adjustments?

- Will banks cope with a greater penetration of fintech, GAFAs and other non-banking providers in the banking market?

- How will future profitability be affected, on one hand, by fast increasing cybersecurity costs and, on the other hand, by possible AI-induced reductions in labour costs?

Situations like the ones just mentioned are not characterized by a very severe combination of macroeconomic conditions and, therefore, do not correspond to the typical stress testing adverse scenario. Instead, the focus is on a narrower and much more focused range of factors that will likely affect the sustainability of the business model over a longer horizon. Sensitivity analysis is a more suitable analytical tool than stress testing for this purpose. It falls in the category of exploratory exercises (Bank of England, 2024) aiming the assessment of emerging risks or structural developments that are not directly linked to the financial cycle.

It is important to distinguish between the different purposes of sensitivity analysis and stress testing. The key distinction is associated with the difference between ‘risk’ and ‘uncertainty’2: stress tests are used in situations where the probabilities attached to future events are known, i.e. we have the conditions to quantify the occurrence of a given set of adverse economic circumstances (‘risk’), typically located in the tail of the distribution; when there is no knowledge of such probabilities, because that type of events has not occurred in the past, it is more common to talk about ‘uncertainty’ and sensitivity analysis.

How should this sensitivity analysis be conducted? Banks should develop baseline projections relying on dynamic balance sheets, accounting for a large set of managerial decisions like business model adjustments, cost-efficiency measures, income diversification, pace of AI adoption. Banks should also produce sensitivity-based projections, according to an economic scenario (or multiple scenarios) provided by the supervisor and, again, by making explicit management decisions. Banks should have full ownership of these projections, which should be subject to thorough supervisory scrutiny (e.g. peer benchmarking and quality control).

This approach is much more realistic than the static balance sheet and, as a result, much more useful as a risk management tool and as a forward-looking planning tool. The design of this exercise has multiple advantages:

- Makes it possible to assess business model viability and sustainability in a comparable way across the banking sector.

- Makes it possible to assess the consistency of banks’ projections over time, as supervisors would be able to identify institutions with more deficient planning procedures such as to not be in conditions to explain differences between projections and outcomes.

- Makes it possible to identify pockets of vulnerability in the business model, if some emerging trends prove to materialize in a faster and stronger way.

Concluding…

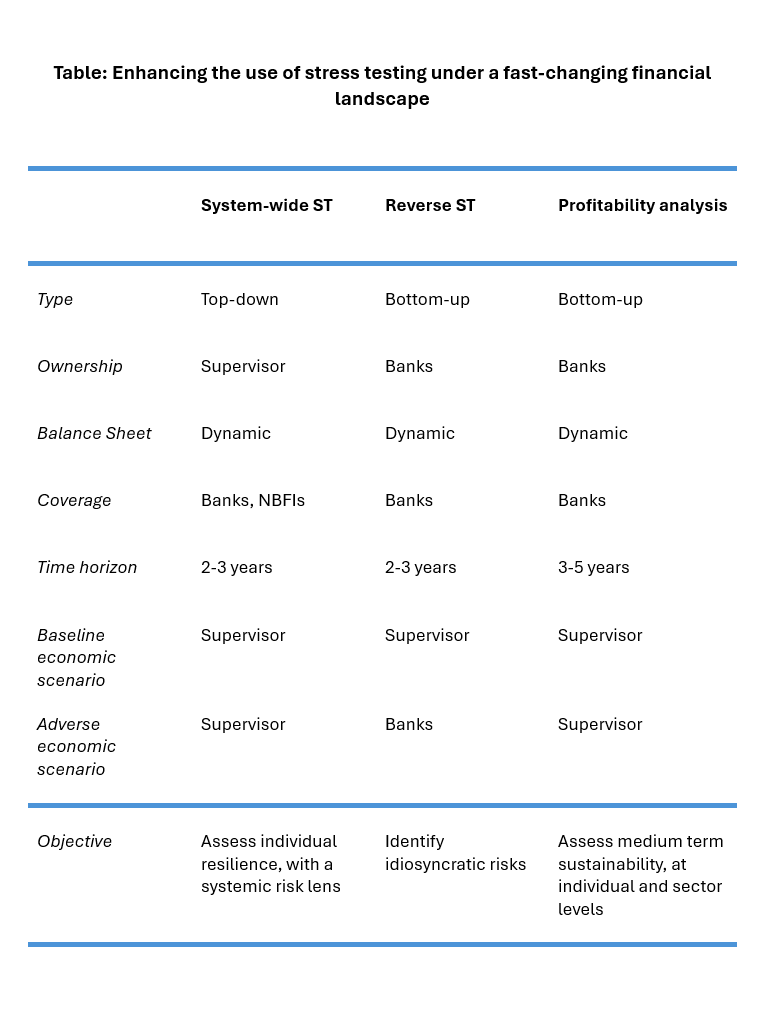

The table below summarizes the most prominent characteristics of the 3 analytical exercises. The system-wide stress test should be top-down and fully owned by the supervisor; both the reverse stress test and the profitability analysis should be bottom-up, relying on banks’ projections, and comprehensively scrutinized and challenged by the supervisor. These 3 exercises should, as much as possible, rely on the use of dynamic balance sheets.

The system-wide stress test should include the largest firms from all the segments of the financial sector ― banks and non-banks ― and the largest leveraged corporates. The reverse stress test and the profitability analysis would be focused on the banking sector. The baseline scenario for the three exercises should be provided by the supervisor and equal for all the participating firms. Running simultaneously the three exercises would benefit from sharing the same baseline economic scenario. The adverse scenarios for the system-wide stress test and for the profitability analysis should be defined by the supervisor, whereas the adverse scenario for the reverse ST should be developed (and justified) by each bank. Finally, the time horizon should be the usual 2-3 years for both stress tests and slightly longer (3-5 years) for the profitability analysis.

The system wide stress test constitutes a capital adequacy exercise, as it assesses how capital ratios would behave in an environment of persistently higher risk premiums and stress in the non-banking sector. Being a common exercise for all the banks it would also be very informative from a systemic risk perspective. The reverse stress test ― which, as a genuine exploratory exercise, provides a mapping of idiosyncratic vulnerabilities (Aikman, 2026) ― is very informative at the individual level and clearly brings extremely relevant information for the micro supervisor. Finally, the profitability analysis provides an assessment of the sustainability of the business model at the individual level, but it also provides very insightful indications for the industry, as it assesses how emerging trends will affect long-term profitability.

The objectives of these three complementary analytical exercises are different. Whereas the system wide stress test and the reverse stress test focus on capital, the sensitivity analysis focus on profitability. Following (Valderrama, 2026) the first two constitute narratives of stocks, whereas the third one is a narrative of flows. Therefore all of them would provide insightful information for the SREP procedure (in the dimensions, respectively, of assessment of risks to capital and business model assessment) through a comprehensive framework that preserves level-playing field across the banking sector.

Author's Note:

- The opinions and conclusions expressed are the authors’ own and do not represent, and should not be reported as representing, the views of Banco de Portugal or the Eurosystem.

Endnotes:

- An economic distinction between uncertainty and risk was proposed by Frank H. Knight in 1921. According to Knight, ’risk is present when future events occur with measurable probability. Uncertainty is present when the likelihood of future events is indefinite or incalculable.’

Pedro Duarte Neves is Adviser for the Board of Directors of Banco de Portugal and editor of the Review of Economic Studies of the Bank. He is a Visiting Professor at Católica Lisbon School of Business and Economics, Associate at the SRC (LSE) – where he is also Editor of the Forum on Financial Supervision – Affiliated Fellow with the Qatar Centre for Global Banking and Finance (KCL), and a member of the Advisory Board of the EBI. He was Vice-Governor of Banco de Portugal, Alternate Chairperson of the EBA, and chair of a number of committees in the scope of the FSB, EBA, and the Joint Committee of the ESAs. He has a vast experience at the main high-level supervisory and regulatory fora, like the EBA, SSM, ESRB, Joint Committee of the ESAs, and FSB. Pedro Duarte Neves published in scientific journals like The Journal of Econometrics, Economics Letters and Economic Modelling. His research interests include banking supervision and regulation, macro-prudential policy, and the real economy.