4th March 2026

Key takeaways

- The growth of investment funds can entail macro-financial benefits, but also requires an evolution in the approach to regulation and supervision to safeguard financial stability.

- At the Central Bank of Ireland, we have responded to the evolution of finance by:

- Increasing our focus on the financial stability implications of the funds sector, in addition to investor protection;

- Developing our approach to surveillance, and adopting policy measures, that recognise the diversity of the funds sector;

- Investing in data; and,

- Given the global nature of capital markets, collaborating with international counterparts on surveillance and policy development.

- Continuing to strengthen the oversight of the funds sector from a financial stability perspective is an important foundation for resilient capital markets.

Main Text

In recent years, a key dimension of the evolution of global finance has been the growing role of non-banks. This structural shift can entail several macro-financial benefits, including diversifying the sources of financing to the economy and strengthening the availability of risk capital to innovative companies. But it also begs the question as to how regulation and supervision need to evolve, to remain effective amid a changing financial system.

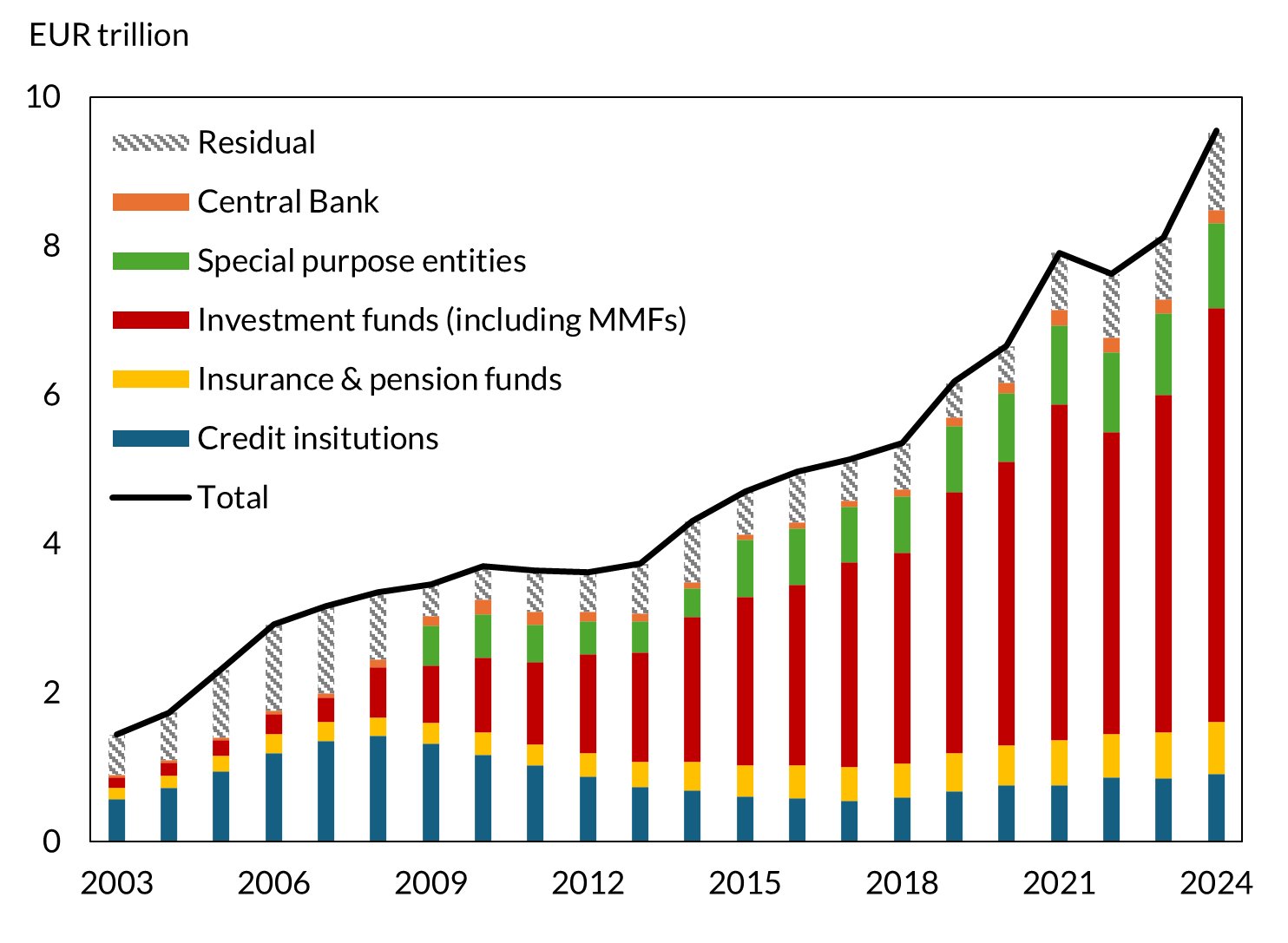

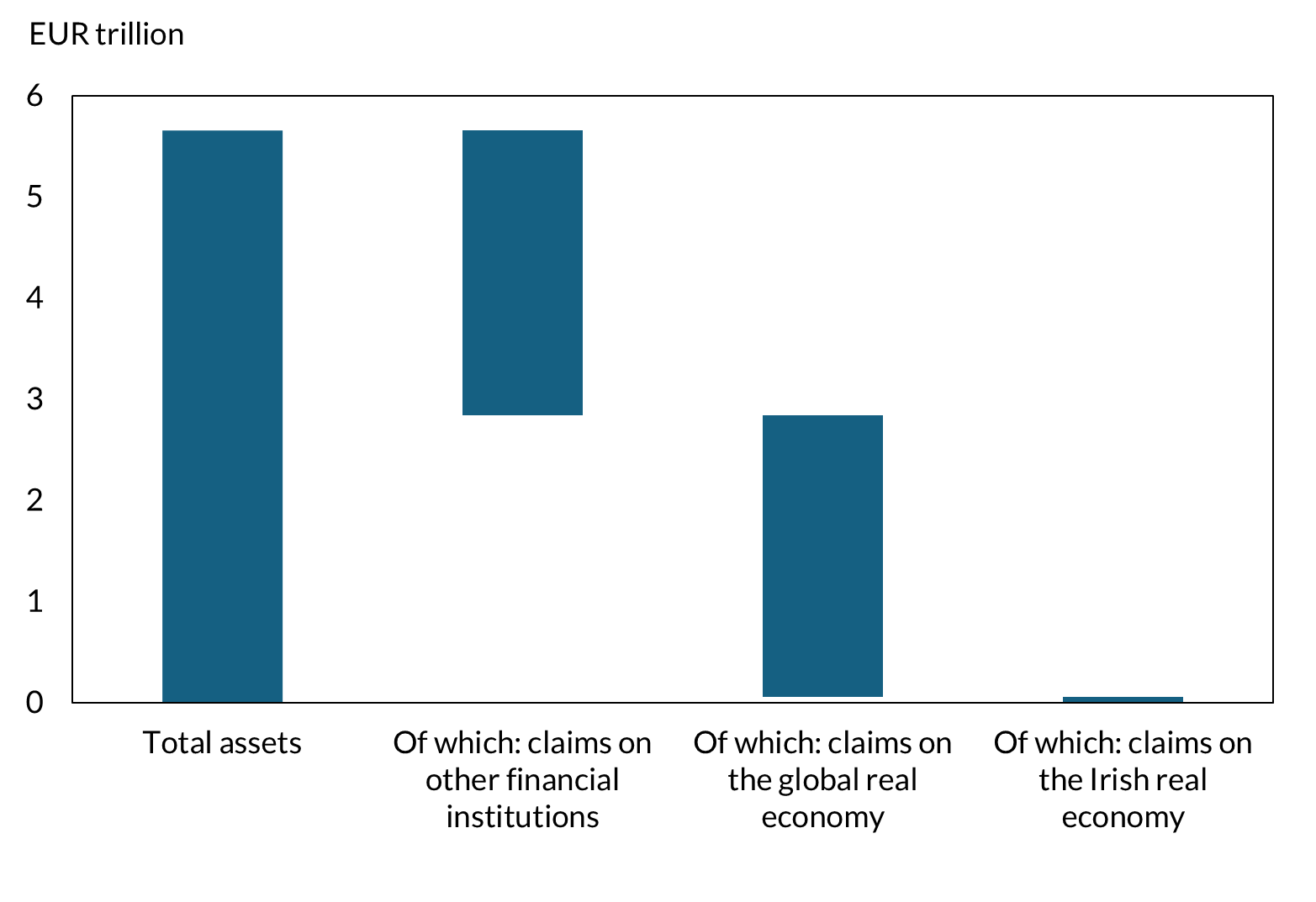

This has been – and remains – at the forefront of our own thinking at the Central Bank of Ireland. In recent years, the growth of the Irish financial system has been driven by the non-bank sector, especially investment funds (Chart 1). By 2024, the funds sector accounted for more than half of total assets of the Irish financial sector. Indeed, Ireland has developed into a global hub for investment fund activity, with the sector providing financing to the European and global financial system and economy (Chart 2).

Chart 1: Investment funds have driven the growth in total assets of the Irish financial system

Source: Central Bank of Ireland and Central Statistical Office.

Notes: Data collection for different subcategories began at different points in time. "Residual" refers to the difference between total assets of financial institutions reported by the CSO and data collected for each of the subcategories.

Chart 2: The Irish funds sector provides substantial funding to the global economy and financial system

Source: Central Bank of Ireland, as of Q2 2025.

As the financial system has evolved, so has the Central Bank of Ireland’s approach to regulation and supervision. The remainder of this post outlines some of the key dimensions of that evolution, with a particular focus on the regulation and supervision of the investment fund sector from a financial stability perspective. It also offers reflections on the path ahead.

A shift in thinking: safeguarding investor protection and financial stability

The growth of the investment fund sector has been a global phenomenon. And it has resulted in an expansion of the market footprint of these entities, across different core markets. For example, global open-ended funds and ETFs are now estimated to account for around 45% of total outstanding US high-yield corporate bonds.1 In the Euro Area, real estate funds account for around 40% of the total commercial real estate market.2 And there has been growing participation by hedge funds in sovereign debt markets in the US and in the Euro Area.3

This growing market footprint means that the investment fund sector is no longer only relevant from the perspective of investors in those structures. It is also relevant for the functioning of core markets. Put differently, if there are underlying financial vulnerabilities in fund structures – for example, stemming from excessive leverage or liquidity mismatch – these can contribute to the emergence of fire sales dynamics in times of stress, which can affect the functioning of core markets and have broader macro-financial implications. The funds sector also has numerous links with other parts of the financial system, including banks.4 This interconnectedness can act as a further channel of propagation of shocks in times of stress.

This is not just theoretical. We saw some of these dynamics first hand in the role that money market funds and certain open-ended funds played in amplifying market pressures during the ‘dash for cash’ episode in 2020 or the role that Liability-Driven Investment (LDI) funds played in the Gilt market disruption in 2022.5 In both instances, extraordinary central bank interventions were required to restore market functioning. These episodes illustrate how vulnerabilities in segments of the funds sector can contribute to markets disruptions. Of course, funds are very different to banks, so the way in which they can contribute to systemic risk is also different.6 Clearly, though, these vulnerabilities have the potential to become macro-relevant.

In that context, a key dimension of the evolution in our approach to regulation and supervision of the funds sector has entailed a shift in thinking. One that recognises that the traditional investor protection lens needs to be increasingly complemented with a financial stability lens. Indeed, the continued evolution of our approach to supervision – across the entire financial system – places particular emphasis on integration: supervising sectors and firms on a holistic basis, across all of our safeguarding outcomes.7

Crucially, this approach recognises that investor protection and financial stability are complementary public policy objectives. At the Central Bank of Ireland – somewhat unusually internationally – we are responsible for both. This has resulted in many internal debates over time, but our experience throughout has been that investor protection and financial stability re-enforce each other. Both are necessary to ensure that capital markets achieve their ultimate economic function of intermediating savings and investment, in good times and in bad.

Broad strokes are not effective, a finer comb is needed

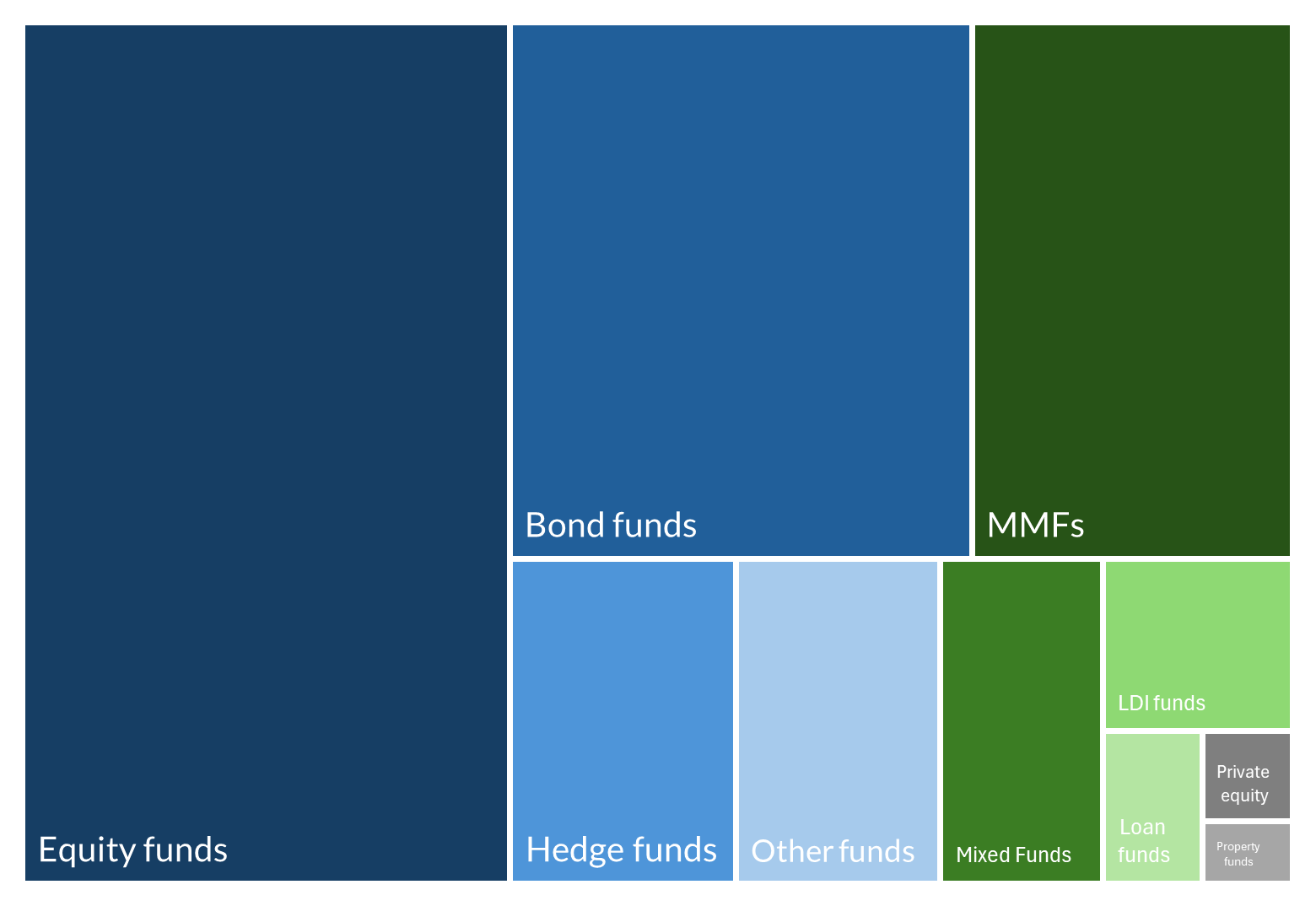

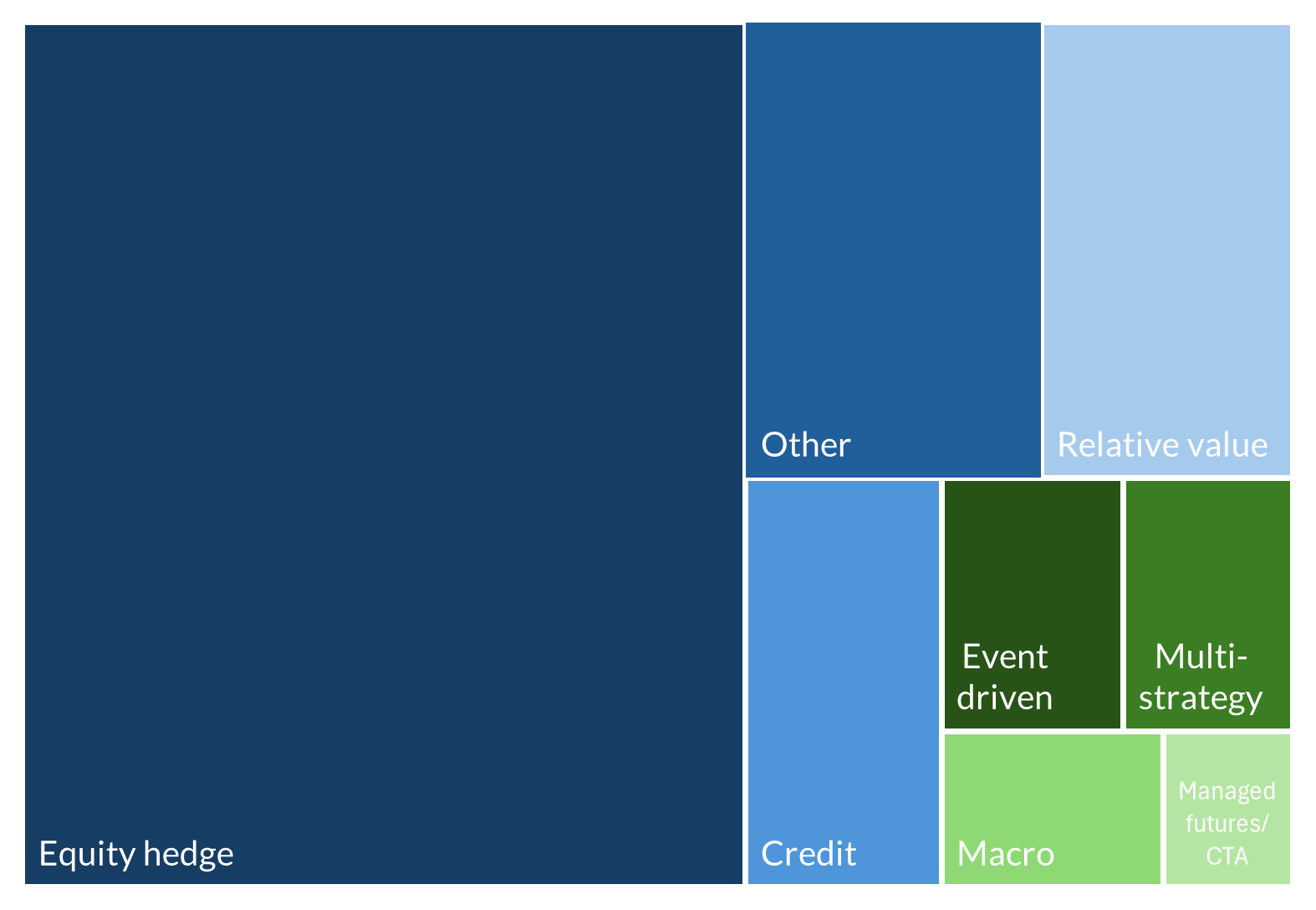

The investment funds sector is very diverse, with funds’ activities varying significantly across entities and products (Chart 3). To state the obvious, money market funds are very different to hedge funds, private credit funds or listed equity funds. The types of investors differ, the characteristics of the underlying assets in which they invest differ, and the investment strategies differ. Indeed, even within a single broad fund category, there can be important differences. An event-driven hedge fund is very different to a relative value one (Chart 4).

Chart 3: The investment fund sector is very diverse, with a range of different fund types

Source: Central Bank of Ireland, as of Q2 2025.

Chart 4: Even within a broad fund category, like ‘hedge funds’, there is significant heterogeneity in strategies

Source: Central Bank of Ireland, as of Q2 2025.

This means that a one-size-fits-all approach to the regulation and supervision of the sector is not effective. Recognising that, a risk-based differentiation of segments of the funds sector lies at the heart of our approach. From a financial stability perspective, our starting point is to monitor potential financial vulnerabilities – whether due to liquidity mismatch, leverage or interconnectedness – across different groups of funds with similar strategies.8 We complement that systematic surveillance with deeper dives into segments of the sector that share similar characteristics. Over recent years, for example, we have conducted deep dives on property funds, hedge funds and liquidity management of open-ended funds.

This approach recognises that the potential financial stability implications do not, in the main, originate at the level of the asset manager. Rather, it is primarily at the level of the fund structures, especially when – in light of common vulnerabilities – funds are responding in a similar manner in response to shocks. This distinction matters. About a decade ago, global policy discussions considered whether to identify asset managers as systemically-important financial institutions. That generated substantial debate at the time and – with the benefit of hindsight, at least – probably delayed progress on addressing system-wide vulnerabilities that might stem from the activities of funds.

The finer comb has also been reflected in our policy interventions. The Central Bank of Ireland has introduced two macroprudential measures to guard against financial stability risks from excessive leverage in two segments of the investment fund sector: property funds and LDI funds.9 These have been targeted interventions, based on detailed analysis of the relevant structures and an assessment of benefits and costs of the measures, to ensure proportionality. The design and calibration of the two sets of measures are very different, reflecting the different underlying characteristics of these two segments of the funds sector – including the assets in which they invest, how leverage is sourced, and how it is managed. Another illustration of the finer comb, recognising that broad strokes would not have been effective.

Investing in data

Data is the heart of risk-based supervision and financial stability analysis and policy. It is key to understanding the entities and markets that we oversee, their features and potential vulnerabilities. And nowhere is that more relevant than in the regulation and supervision of the funds sector. That is partly due to the industrial organisation of the sector. While there is a relatively small number of asset managers, there are approximately 9,000 funds authorised in Ireland. It would not be possible to supervise the sector effectively, in the absence of good data.

This is something that we have recognised over a number of years, and have – and continue to – invest significantly in. Part of that investment reflects efforts by the European System of Central Banks to strengthen our collective understanding of the financial system as a whole, through enhanced statistics. Another part reflects the evolution of European-wide supervisory reporting requirements for the funds sector. Being both a central bank and a supervisory authority allows us to combine this information – something that may be more difficult in some other jurisdictions, where the central bank and supervisory authority are separate entities.

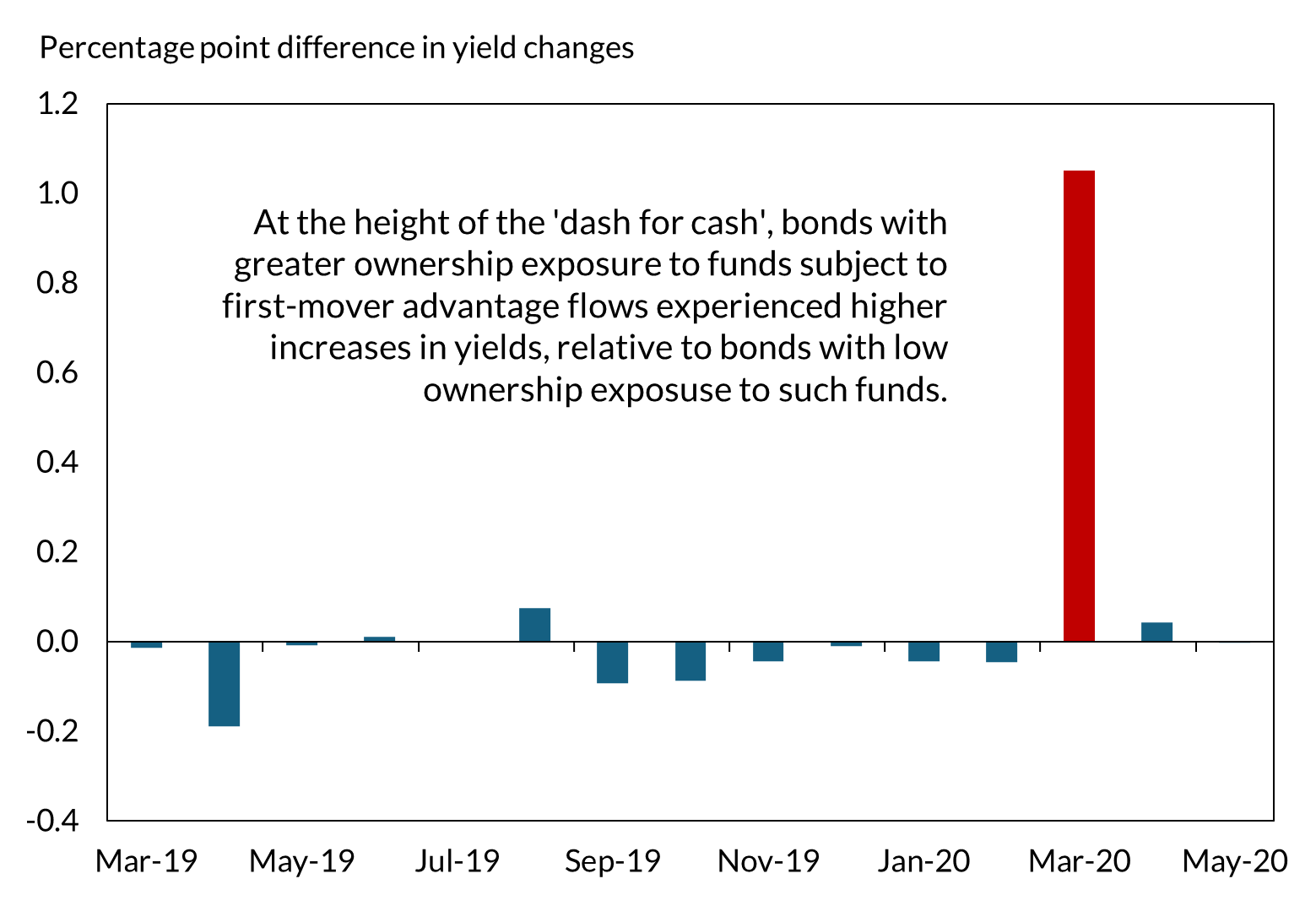

And we see the benefits of combining this information first hand. For example, we are able to combine metrics around leverage or liquidity mismatch of individual funds (based on supervisory data), with data around the securities holdings of those funds (based on statistical data). That allows us to connect potential financial vulnerabilities to the market implications of these vulnerabilities (Chart 5) – which is at the heart of the ‘shift in thinking’ to include the financial stability lens in the regulation of investment funds. And is also allows us to conduct deeper analysis and research, which is a cornerstone of understanding the macro-financial implications of the evolution in the financial system.

Chart 5: Financial vulnerabilities in the funds sector can amplify macro-financial shocks in times of stress

Source: Chen and Dunne (2024) ‘First-mover advantage in funds revisited’, Central Bank of Ireland Research Technical Paper, Vol 2024, No. 6.

We have also complemented those European data initiatives with targeted additional collections, where we have judged that it is proportionate. For example, we collect data on daily redemption and subscription flows as well as on the availability and use of liquidity management tools. These have been important enablers of our risk-based supervisory approach. For example, at the height of the market turbulence of April 2025, we were able to monitor liquidity flows across the funds sector and better target our supervisory engagement around liquidity management to those segments of the funds sector that were experiencing larger redemptions flows.10

In the policy discussions around non-banks, I sometimes hear references to opacity and lack of data. This is another example where a broad brush is not helpful. While opacity is certainly a challenge in some segments of the non-bank sector, such as private credit funds or hedge funds, it is not a consistent feature across the regulated funds sector. Of course, there are still data gaps that need to be filled, but our focus needs to be prioritised. Overall, over the past decade, we have made important strides in collecting and analysing data that help us better understand the vulnerabilities of the funds sector and its interconnections with the broader economy as well as other parts of the financial system.

Global solutions to global challenges

Capital markets are global in nature. This – in and of itself – entails significant benefits for the global economy, enabling the flow of capital across borders. It is therefore not surprising that the funds sector has very significant cross-border exposures. International co-ordination in the regulation and supervision of the funds sector is therefore critical. In that context, global bodies – such as the Financial Stability Board (FSB) and the International Organization of Securities Commission (IOSCO) – play a particularly important role.

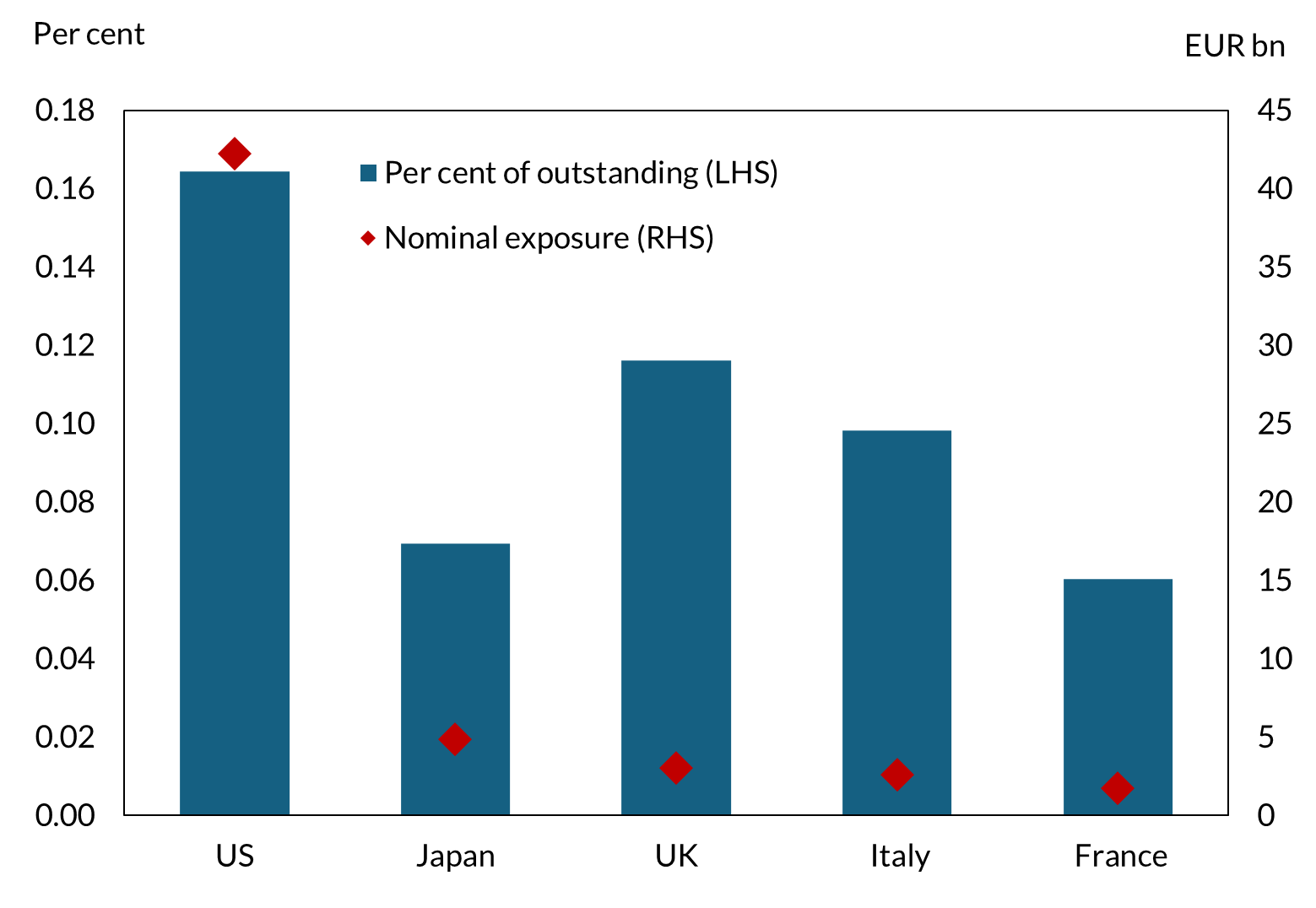

One important dimension of global co-ordination is around surveillance, which is the backbone of any risk-based supervisory approach. Ultimately, each jurisdiction sees just a piece of the global puzzle of international capital markets. To be able to understand the full picture, we collectively need to put together all the pieces of the puzzle. Let me give one tangible example here. Our ongoing deep dive on hedge funds has shown that holdings of sovereign debt by Irish-resident hedge funds are relatively limited, when compared to the total outstanding amount of sovereign debt securities (Chart 6). But there are similar funds, with similar strategies, and similar exposures, in other jurisdictions. We can only understand the macro-financial effects of increased hedge fund participation in sovereign debt markets by considering the collective response of the global hedge fund sector to adverse shocks. This is why the work of the FSB (at a global level) and the ESRB (at a European level) to coordinate surveillance is so important.

Chart 6: Holdings of sovereign debt by Irish-resident hedge funds are limited, relative to the total outstanding

Source: Central Bank of Ireland, BIS debt securities statistics, and Central Bank of Ireland calculations as of Q2 2025.

Note: Values examine direct on-balance sheet exposures only. Indirect exposures via holdings of funds in other jurisdictions, feeder funds for master funds in other jurisdictions or synthetic exposures are not examined. Market share estimates use Closing Position of the market value of General Government Debt from the BIS Debt securities statistics.

Another important dimension of international co-ordination is around policy and supervisory responses to identified vulnerabilities. In the absence of that, risks could just shift across borders, limiting the effectiveness of any regulatory intervention. Following the ‘dash for cash’ episode in March 2020, the FSB and IOSCO progressed a number of policy initiatives to strengthen the resilience of the non-bank sector, including in relation to liquidity management by money market funds and open-ended funds, as well as leverage-related risks amongst non-bank financial institutions (including funds). Yet the implementation of these recommendations remains uneven across jurisdictions.11 More needs to be done to progress implementation in a consistent manner across the world, including in Europe.12

The Central Bank of Ireland has been a strong advocate for international co-ordination in the regulation and supervision of investment funds. We are active contributors to the FSB’s and the ESRB’s work to monitor trends in non-bank financial intermediation. While Ireland is not a member of the FSB, given the nature of the sector in Ireland, we have contributed to the policy work of the FSB and IOSCO around money market funds, open-ended funds and leverage in the non-bank sector. International co-ordination has also been central to specific regulatory interventions we have taken. For example, the measures that we introduced to safeguard resilience of LDI funds were designed in close co-ordination with the markets authority of Luxembourg, ESMA and UK authorities.

Ultimately, financial stability and investor protection are global public goods. Everyone benefits from resilient and well-functioning global capital markets. And delivering global public goods relies on effective co-ordination at an international level.

Looking ahead

While, in recent years, there has been significant global focus on strengthening the oversight of the investment fund sector from a financial stability perspective, this is an ongoing journey. In that context, let me outline what I think are three broad priority areas going forward.

First, developing a global approach to sharing of information and data, across jurisdictions and across authorities. As I mentioned above, data is an essential enabler for effective surveillance. Yet there are still frictions and barriers to the sharing of information and data at a global level. That limits authorities’ collective ability to put together the pieces of the global puzzle and evaluate the evolution of potential vulnerabilities in international markets. In that context, it is encouraging that the FSB has set up a task force on non-bank data, which – among others – is also exploring whether and how authorities could share information, including data, when this could be used to mitigate significant threats to financial stability. This is not easy. But the potential rewards can be very large, both from the perspective of authorities as well as globally-active regulated entities, which currently may have to provide broadly similar information, to different authorities, in different formats.

Second, strengthening our approach to identifying vulnerabilities in the investment fund sector that are – or have the potential to become – macro-relevant. From a financial stability perspective, it is important to focus our collective efforts on macro-relevant vulnerabilities. That is a key guiding principle, to guard against the risk of missing the wood for the trees, amidst a very diverse sector. Reaching a judgement on what is macro-relevant requires an understanding of the interactions between financial vulnerabilities in segments of the investment fund sector and other parts of the financial system or the broader economy. An innovative approach for evaluating those interactions has been the Bank of England’s system-wide exploratory scenario. By focusing on the functioning of core markets, this approach is well placed to identify potential macro-relevant vulnerabilities. This is a toolkit that could be usefully expanded elsewhere, including in Europe as well as, ultimately, at a global level.

Third, building on the above, developing the analytical framework for evaluating system-wide policy measures to safeguard resilience in markets. If material macro-relevant vulnerabilities are building, we should not wait for stresses to emerge before taking action. An ounce of prevention is worth a pound of cure. Of course, amid an evolving financial system, delivering such an ex ante strategy is not straightforward. The case for policy intervention can appear less compelling if stresses have not yet crystallised in a newer, growing segment of the financial system. Developing the analytical framework for evaluating the need for system-wide policy measures in markets can help regulators globally reach those judgements ex ante. Indeed, not intervening is as much a decision – with associated benefits and costs – as intervening. It needs to be an explicit judgement, based on evidence and analysis. And, where system-wide policy measures are introduced, such analytical frameworks can inform policymaker judgements around proportionality, balancing benefits and costs.

To sum up, an increasing role of non-bank financing can entail many macro-financial benefits. Indeed, in Europe, there is – rightly – renewed focus on strengthening the role of capital markets to complement bank-based financial intermediation. Investment funds are core to capital markets activity and, therefore, to strengthening the role of capital markets in Europe. Ultimately, though, for the benefits of increased capital market activity to be realised, this form of financial intermediation needs to be resilient. If it is not, companies will not want to rely on capital markets for financing. And households will not want to use those markets to channel their savings. The opportunity lies in developing capital markets that serve the economy in a sustainable way: in good times and in bad. Continuing to strengthen the financial stability lens in the regulation and supervision of the funds sector is an important foundation for that.

Endnotes:

- See IMF (2025) ‘Global Financial Stability Report’, available here.

- See Daly et al (2023) ‘The growing role of investment funds in euro area real estate markets: risks and policy considerations’, Macroprudential Bulletin 20, available here.

- See Sushko and Todorov (2025) ‘Sizing up hedge funds' relative value trades in US Treasuries and interest rate swaps’, BIS Quarterly Review, December, available here; Barth et al (2025) ‘The cross-border trail of the Treasury basis trade’, FEDS Notes, available here; and Ferrara et al (2024) ‘Hedge funds: good or bad for market functioning’, ECB Blog, available here.

- See, for example, Bochmann et al (2025) ‘Systemic risks in linkages between banks and the non-bank financial sector’, ECB Financial Stability Review, available here.

- See FSB (2020) ‘Holistic review of the March market turmoil’, available here; Pinter (2023) ‘An anatomy of the 2022 Gilt market crisis’, Bank of England Staff Working Paper, No. 1019, available here; and Dunne et al (2023) ‘Irish-Resident LDI Funds and the 2022 Gilt Market Crisis’, Central Bank of Ireland Financial Stability Note, Vol. 2023, No. 7, available here.

- For a discussion of the channels through which investment funds can contribute to systemic risk, see Central Bank of Ireland (2023) ‘An approach to macroprudential policy for investment funds’, available here.

- See Central Bank of Ireland (2025) ‘Our approach to supervision’, available here.

- See, for example, Central Bank of Ireland (2024) ‘Market-based finance monitor’, available here.

- Central Bank of Ireland (2022) ‘The Central Bank’s macroprudential policy framework for Irish property funds’, available here; and Central Bank of Ireland (2024) ‘The Central Bank’s macroprudential policy framework for Irish-authorised GBP-denominated LDI funds’, available here.

- See, for example, Central Bank of Ireland (2025) ‘In focus: The Irish NBFI sector during the April market volatility episode’, Financial Stability Review, available here.

- FSB (2025) ‘G20 Implementation Monitoring Review: Interim Report’, available here.

- See, for example, the Eurosystem’s response to the EU Commission’s consultation on macroprudential policies for NBFI, available here.

Vas Madouros is Deputy Governor, Monetary and Financial Stability, at the Central Bank of Ireland. In this role, he oversees the Economics & Statistics, Financial Stability and Financial Operations Directorates, and is an ex-officio Member of the Central Bank’s Commission. Prior to joining the Central Bank of Ireland, he was at Bank of England, where his work spanned macro-prudential policy development, stress testing, international finance, prudential policy and macro-financial risk assessment.