23rd June 2026

Key takeaways

Economic risks are seriously under-estimated because of the failure to monitor and diagnose trends in the land and rent markets. The author claims that lawmakers intentionally ignore the cyclical trends driven by the combination of property rights and fiscal policies. To navigate looming global crises, revisions are needed to the way governments raise revenue. Diminishing the economic risks would enhance the resilience of society, generating greater cooperation and consensus about the policy instruments that best serve democratic governance.

Rent induced Recessions: When risk is not a risk

Within statecraft, problems that require the attention of law-makers seemingly arise from one of two sources. The random events cannot be anticipated with precision. The structurally induced events ought to be anticipated, if knowledge is sufficiently advanced for law-makers to understand how the system works; which would enable them to apply preventative action. But, there is a problem with allotting certain socially significant problems into either of those two categories. There is a third set of problems: those that stem from wilful blindness.

Is poverty (for example) a random or structural issue? What if it can be eliminated, by empowering everybody to work for wages that meet their metabolic needs; but governance chooses not to apply the appropriate remedial measures? In that case, we cannot hold random or structural forces responsible for poverty. Similarly with business cycles. If we can predict them, and if the remedial policies exist, it would not be appropriate to attribute them to random or structural causes. If such risks do exist, we need to classify them within a separate category: wilful blindness.1

But would a rational, science-based society tolerate such a third group of problems – especially societies based on universal suffrage? The answer, I fear, is “Yes!” Policy-makers do grapple with issues that could be erased, but which they choose not to remediate. In their origins, those issues stem from the failure to synchronise the two pricing systems at the interface between the market economy and the public sector. And if that is the case, responsibility must lay with the law-makers, who possess the power to harmonise the relationships between the public and private sectors. I will illustrate this issue in relation to the business cycle, the one that occurs every 18 years, and is shaped by policies that discriminate in favour of rent-yielding assets.

Pricing mechanisms

In a rational world, people would allocate their resources to fund personal consumption and social need on terms that fulfilled their aspirations. This proposition presumes that people would confine their demands to realistic parameters: expectations confined within the limits of what they were willing to produce, to fund daily metabolic needs, and the requirements that have to be funded through public agencies. That would ensure no disconnect between supply and demand in either the private or public sectors. But the current social system operates with tax policies that rupture the capacity to produce the optimum levels of revenue needed to fund the services shared in common. Fiscal policy disconnects the public and private sectors; even though people do, in fact, produce sufficient income to meet all of their realistic aspirations.

The disconnection arises because the fiscal system generates two consequences. First, taxation dislocates people’s productivity, in both the labour and capital markets. Taxes on the earned incomes from labour and capital impose “deadweight burdens”. Second, the fiscal regime privileges the owners of rent-yielding assets. The bias results from variations in the relative powers of the three productive factors (land, labour and capital). Technically, that power is known as “elasticity”, which measures the responsiveness of one economic variable to changes in other variables. Ordinarily, land exercises the greatest influence within a market, because “they ain’t making any more of it”. Land cannot be readily created (increased in supply). This compares with an increase in demand for capital (which can be readily reproduced), or for labour (which, all else failing, can be imported from abroad).

If (as is the case) public policy does not neutralise the power advantage enjoyed by rent-yielding assets, economic outcomes are biased to favour the owners of land. Superimposed on this bias, are the taxes on earned incomes that burden labour or capital (which result in sub-optimum levels of productivity). The absence of a direct fiscal charge on rent, to neutralise its elasticity advantage, creates a competitive advantage for the owners of rent-yielding assets.

From this, it follows that, no matter how diligently a population works to fulfil its needs, supply will not equate with demand. That is because a significant part of national income is diverted. In economics, economic rent is called a “transfer income”. The most visible manifestation of this, are the rents of location (as in: land owners). Those owners can claim rents even if they do not own the asset that generates the rents. An example is the rental value of the electromagnetic spectrum. Those rents are collected by the owners of internet platforms, even though they do not own the spectrum. Spectrum rents end up in the pockets of those who own the digital platforms, by default: governments fail to impose a rent charge, within their domains, for the use of that natural resource.

One outcome, in the private sector, is involuntary poverty. Another outcome, in the public sector, is the inability to fund all of people’s social needs; resulting in sovereign indebtedness.

But how does this result in predictable, 18-year cycles?

The recurring cycles

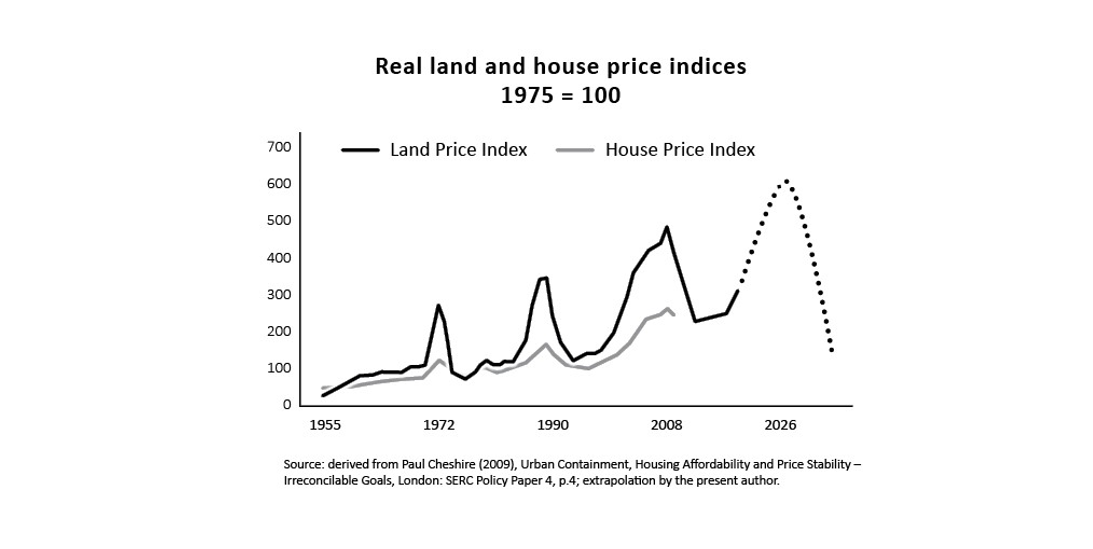

Except for the intrusion of an overwhelming event (like a world war), for centuries the market economy has been disrupted every 18 years by serious recessions. These were first identified in the 1930s by Homer Hoyt in his doctoral research. He traced the pattern in the Chicago land market.2 I subjected Hoyt’s findings to a cross-country/cross-cultural analysis (primarily, the USA, UK, Australia and Japan) to verify that the phenomenon was not peculiar to Chicago real estate.3 I also confirmed that, once the disruptions from food rationing and the Korean war were out of the way, following World War 2, the UK’s 18-year cycle reasserted itself (see Fig. 1) The end of the first cycle was 1972. Fig. 1 tracks the three post-war cycles; and I have extrapolated it to include the current cycle. The rent cycle stalls in 2026, terminating in the recession and the current business cycle in 2028.

Fig. 1

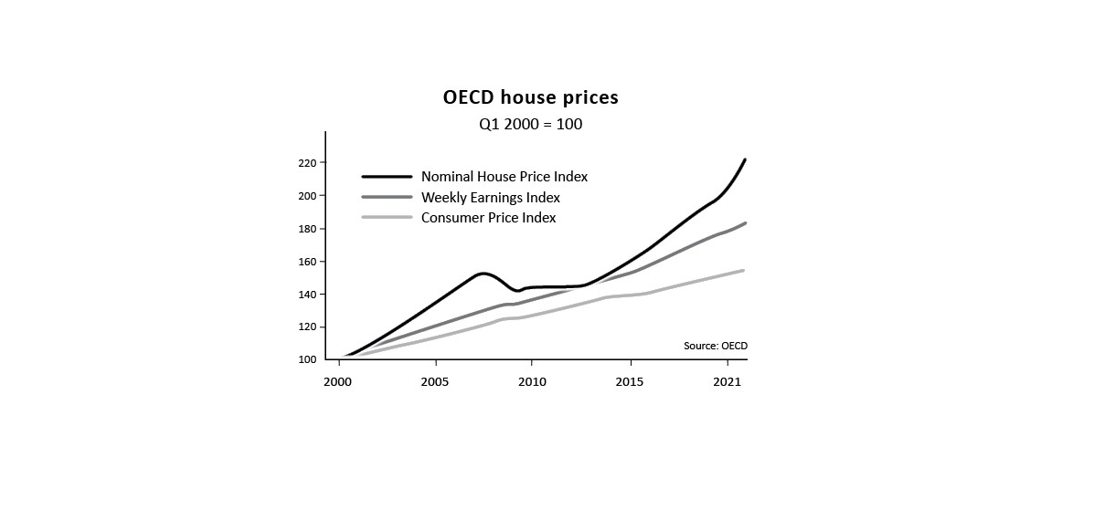

That the 18-year cycle is repetitive, was confirmed by the real-time test I applied during the third of those post-war cycles. When Tony Blair’s New Labour Party was elected in the 1997 election, I wrote to him to explain that house prices would peak in 2007 (“house prices” being a proxy for land rents), followed by a severe recession. At the same time, I wrote in similar terms to Chancellor of the Exchequer Gordon Brown; to the First Secretary of the Treasury; to the Press Secretary in Downing Street, and to Peter (now Lord) Mandelson, the architect of the Third Way manifesto. I recorded my prediction in a book published in 1997,4 and repeated the forecast in 2005.5 House prices peaked in the final quarter of 2007, and the Queen asked her famous question – “Why did nobody see it coming?” – in November 2008, during her visit to the LSE. In 2010, I summarised this empirical test in The Inquest.6

Was my 1997 forecast based on luck? According to Paul Kennedy, a British-born history professor at Yale, correctly forecasting the future is based on luck.7 We can test Kennedy’s proposition in relation to the current 18-year cycle. If it is to end in 2028, the rise in “house prices” (taken as the proxy for location rents) should end in 2026. We can see from Fig. 2 that house prices monitored by the OECD have outpaced earnings and consumer prices over this period; which suggests a squeeze on spending power that prejudices the macro-economy.

Fig.2

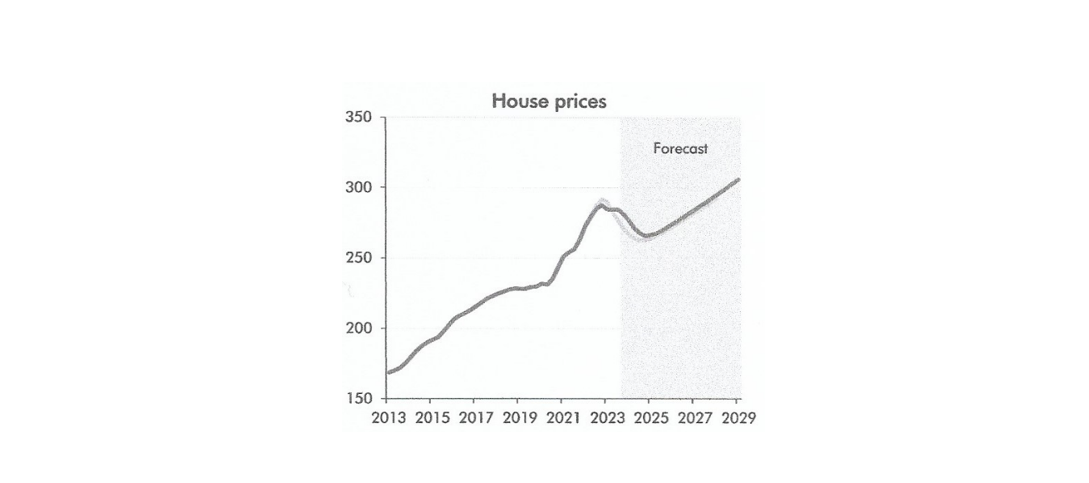

According to the UK’s Office for Budget Responsibility (Fig. 3), Britain is not hovering at the precipice of a house price-inducted crash. It forecasts growth in house prices all the way through to 2029.

Fig.3

Is the blindness wilful?

But, to sustain the proposition that statecraft is wilfully biased against rational fiscal arrangements, I need to demonstrate three issues. First, a viable fiscal solution to the boom/bust cycle exists. Second, that influential voices in the realm of economic theory have wilfully turned blind eyes on “the land question”. And, third, that HM Treasury refuses to contemplate the one fiscal policy that would address instabilities in the market economy.

On the viability of a fiscal reform that would harmonise the private market and social sector into a holistic relationship, the evidence dates back to Adam Smith. In The Wealth of Nations he provides ample theoretical arguments in favour of shifting the tax regime in favour of collecting revenue directly from rent. His work was amplified through the 19th century by philosophers like J.S. Mill, and in the 20th century by Nobel Prize economists like Joseph Stiglitz.

On the second issue, that economics is wilfully blind, the closest we can get to a confession was provided by J.M. Keynes. Following the classical 3-factor model of economics that originated with Adam Smith, the 20th century saw the birth of the neo-classical 2-factor (labour and capital) model. Land, and rent, were buried as sub-categories of “capital”, despite the unique characteristics that distinguish land from capital.

Classical theory came to a grinding halt in Parliament. A Liberal government tried to enshrine a direct charge on rent in its 1909 budget. This was defeated. Following the constitutional crisis, the Liberals succeeded to impose the charge in their 1910 People’s Budget. However, despite the eloquent support rendered by people like Winston Churchill, the policy was revoked in 1920. And so we come to Keynes. In 1925, while drafting his thesis on the relationship between governance and the economy, he posed the question of which issues ought to preoccupy policy-makers.

Some will say — the Land Question. Not I — for I believe that this question…has now become, by reason of a silent change in the facts, of very slight political importance.8

Even as he penned those words, frenetic land speculation was driving up the price of Florida’s sand dunes to astronomical levels, triggering the land boom that provoked the stock market Crash of ’28.9 That led, in turn, to the Depression of the ’30s.

Finally, what of the attitude within HM Treasury, where policy is actually implemented? For an insider’s testimony, we cannot do better than turn to Nicholas (now Lord) Macpherson. He served HM Treasury as chief economist before his elevation to Permanent Secretary. During his 30 years at the heart of government, administering the collection of revenue to fund the state, he endured an abiding discomfort.

It worries me…that we don’t have a land tax. In a sane world, we would have a proper land tax. Sadly the only person to try it was Lloyd George and he ended up having to pay every single penny back. 10

Macpherson revealed the pathology that even prevented discussion of Rent as a source of public revenue. When he raised the subject of a tax on land within the Treasury, his colleagues treated him as if he was “insane”.11 “I tried my best to get successive governments interested in the taxation of land and property. But sadly I failed!”12 Few public servants have been as honest as Nick Macpherson (see Box).

A rare Confession Within days of retiring from HM Treasury, Macpherson confessed. As head of the Treasury in its darkest days, he admitted he was among those guilty of a “monumental collective intellectual error” in the run-up to the 2008 crisis, which is characterised as a financial crash. “I see myself as one of a number of people in finance ministries, central bank regulators, in the UK and the US who failed to see the crisis coming, who failed to spot the build-up of risk,” he admitted. “This was a monumental collective intellectual error.”* * George Parker (2016), “Veteran of Treasury battles tots up a decade’s wins and losses”, Financial Times, April 14. |

These foregoing examples may appear to be random selections to fit the thesis: the full documentation appears in my book, Cheating. 13

The ripple effects

One consequence of the wilful blindness syndrome is that national statistical agencies have little reason to assemble good data on land and rent. The need for such data is in plain sight. An IMF working paper acknowledges that “unbalanced developments in real estate markets can also be an important factor contributing to vulnerabilities and possibly crises in the financial sector”. The authors note, however, the “lack of good quality and timely data [from] real estate markets”. Most international databases “do not include real estate indicators – such as prices, rents, vacancy rates, construction costs, real estate lending, and stock prices of real estate companies”.14

The ripple effects emanating from the fiscal bias are legion. They include, for example, the contraction in the aggregate demands of consumers (many of whom are forced to pay increasing proportions of wages to fund mortgages); and the increased pressures on government budgets (to fund rising demands from those forced into poverty). These effects amplify the down-the-line dislocations that preoccupy law-makers with their palliative policies that do not work, but with which they persist.

The cyclical recessions that originate in the land market are not a risk, in the usual meaning of that word. They are predictable; can be insured against; and can even be eliminated, if the democratic will existed.

Last time, when the Queen posed her challenging question, the end of the rent-induced cycle was camouflaged as a “financial crisis”. If King Charles was to repeat his mother’s question, in 2028, what should he be told?

Author's Note:

- Director, Land Research Trust, London. Fred.geophilos@gmail.com

Endnotes:

- One consequence of wilful blindness (in the present author’s view) is that “values for land supply elasticities are rarely available in the literature”. Andrzej Tabeau et al (2017), Land Supply Elasticities: Overview of available estimates and recommended values for MAGNET, Luxembourg: European Commission, p.4.

- Homer Hoyt (1933), One Hundred Years of Land Values in Chicago, Chicago: University of Chicago Press.

- Fred Harrison (1983), Power in the Land, London: Shepheard-Walwyn

- Fred Harrison (1997), The Coming ‘Housing’ Crash”, in Frederick J. Jones and Fred Harrison, The Chaos Makers, London: Vindex, p.27.

- Fred Harrison (2005), Boom Bust: House Prices, Banking and the Depression of 2010, London: Shepheard-Walwyn.

- Fred Harrison (2010), The Inquest, London: DA Horizons.

- Paul Kennedy (1988), The Rise and Fall of the Great Powers, London: Harper Collins, p.565.

- J.M. Keynes (1925), “Am I a Liberal?” The Nation and Athenæum, Aug. 8 and 15.

- https://fcit.usf.edu/florida/lessons/ld_boom/ld_boom1.htm

- https://slrg.scot/blog/wp-content/uploads/2019/01/PB3.web_.pdf

- https://slrg.scot/blog/wp-content/uploads/2019/01/PB3.web_.pdf

- Personal communication to the present author, June 5, 2023.

- Fred Harrison (2026), Cheating: The Human Project and its Betrayal, London: Shepheard-Walwyn.

- Paul Hilbers et al (2001), Real Estate Market Developments and Financial Sector Soundness, IMF WP/01/129, p.28.

By profession a journalist, Fred Harrison took leave of absence from Fleet Street to study for degrees at Oxford and London universities. He then embarked on a career as economic consultant. His first book, The Power in the Land (1983), provided the evidence enabling him to offer 10-year forecasts of the downturns of 1992 and 2008. During the 1990s, he worked with the head of the economics department of the Russian Academy of Sciences to explain to the Yeltsin government that Russia was ideally placed to adopt the Adam Smith model that combined ethical economics with authentic democratic governance. His failure convinces him of the need to revise much of economic language. His latest book, Cheating: The Human Project and its Betrayal, traces the institutionalised origins of poverty and inequality back to antiquity, to explain why injustice is enshrined as a structural feature of modern societies.