8th July 2025

Andrea Resti’s contribution opens the section of the Forum focused on real estate, discussing the risks and segmentations as well as the role of non-bank financial institutions in EU markets1

Key takeaways

- Mortgage loans show too many national segmentations across EU Member States regarding the role of floating-rate loans (still too high in some jurisdictions) and the average cost of home loans. Such asymmetries should be further investigated with a view to promoting efficiency and effectiveness.

- Segmentations also exist regarding lending standards. Differences exist in the minimum levels of debt-sustainability indicators, lending products and property evaluation practices.

- Non-bank financial institutions play a major role in real estate financing. Real estate funds in the euro area are still a patchwork of national practices and rules. Contagion channels to and from other institutional investors should be monitored through transparent and uniform reporting.

Foreword

Real estate risks play a major role in the banking sector, as shown by a large number of financial crises, including the 2007-2009 Great Financial Crisis (GFC). This is due to several mutually reinforcing characteristics of real estate-related exposures: first, they are vulnerable to numerous macroeconomic factors (market prices, interest rates, unemployment rates in the case of residential mortgages, aggregate demand for commercial real estate investments) that jointly affect a large number of borrowers, creating “waves” or “clusters” of defaults, that lead to a quick build-up of risks; secondly, rising property values lead to abundant bank lending, but this link may quickly reverse as banks become more cautious following a price correction (raising lending spreads or tightening origination standards), depressing demand and leading to further price corrections and downward spirals2.

In the EU market, the last three years have marked a sudden shift from a “lower for longer” interest rate scenario in 2015-2022 to a sharp increase in the cost of debt (including for fixed-rate exposures that needed to be rolled over). Although 2024 and early 2025 have marked a reduction in money market rates, improving the affordability of property loans, real estate risks still rank high in the supervisors’ agenda3.

This paper reviews some recent data on property markets and related bank loans in the euro area, looking at prices, credit quality and the costs faced by borrowers. We then take a closer look at some possible improvements in the origination and monitoring practices of some euro area significant institutions, as recently analysed by the ECB. Finally, we turn to property-related exposures held by non-bank financial institutions (“NBFIs”), focusing on the main vulnerabilities shown by real estate investment funds.

Real estate risk in the euro area: where do we stand?

Property prices and mortgages in the euro area

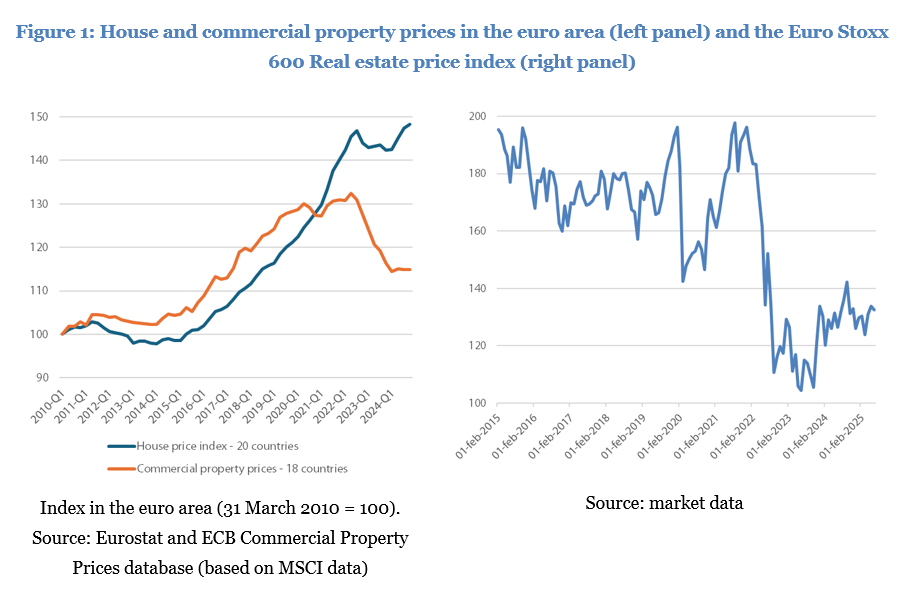

In 2016-2019 (see Figure 1, left panel), real estate prices in the euro area have experienced four years of steady growth, also in response to looser lending standards (as indicated, e.g., by higher loan-to-value ratios for residential property4). In the following years, prices for residential and commercial real estate (“RRE” and “CRE”) have taken diverging paths: the former have kept rising throughout the Covid-19 pandemic (2020-2021), accompanied by a further easing of lending conditions5, whereas the latter have been negatively affected by the drop in economic activity and the shift in demand across economic sectors (due to, e.g., lower appetite for office buildings and shopping malls). In 2022-2023, the quick rise of interest rates led to a drop in new mortgages, cooling down the market for residential property6, while CRE – being largely dependent on leveraged finance - witnessed a sharp decline in prices.

Although concerns about the real estate sector have somewhat eased in 2024, market valuations remain very cautious, with the STOXX 600 Europe Real Estate Index remaining well below the levels experienced during the pandemic (see Figure 1, right panel)7.

Credit quality and the effect of higher interest rates

Although per-capita home loans and the weight of mortgages on total bank loans differ greatly across EU Member States8, loans secured by real estate account for roughly one third of total bank loans in the euro area9, with a higher incidence for households (24% of total bank loans) than for non-financial companies (10%).

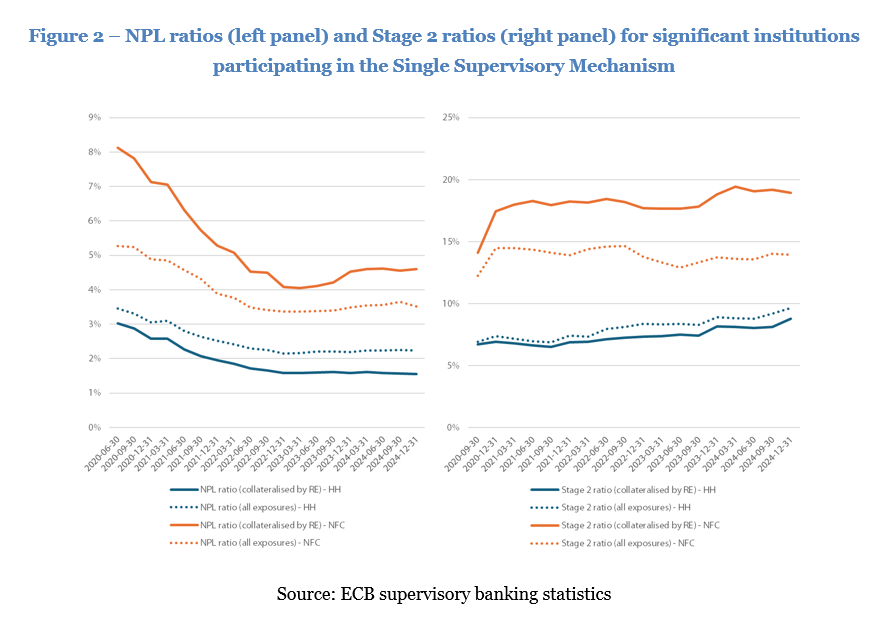

Credit risk indicators for bank loans collateralised by real estate remain under control for Significant Institutions (SIs) in the Banking Union (see Figure 2): the NPLs ratios of households and non-financial companies have indeed shown a decreasing profile since mid-2020, although the latter have experienced a small rebound since 2022. The Stage 2 ratios10 have been increasing throughout the last four years, especially for NFCs, which may be assumed to include most loans secured by commercial real estate.

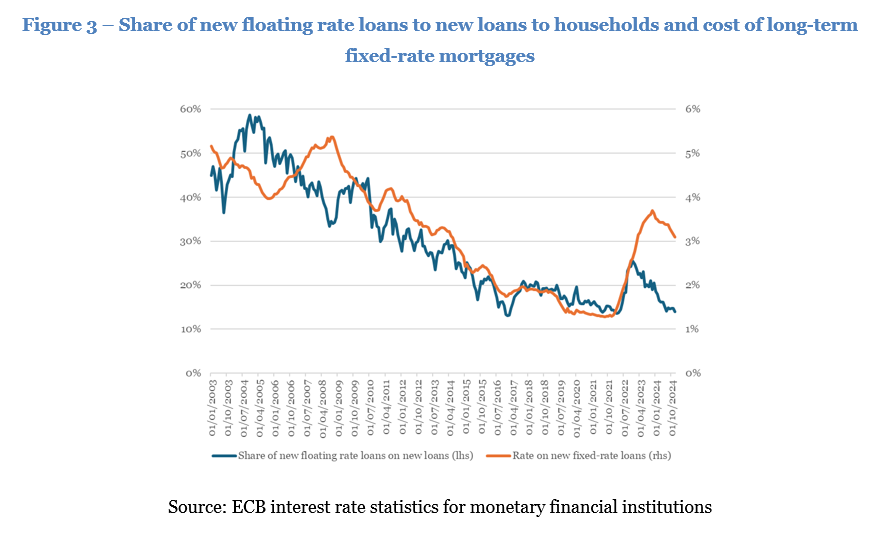

As far as residential mortgages are concerned, the impact of higher interest rates has proved manageable due to two mutually reinforcing phenomena (see Figure 3). On one hand, until mid-2021, new floating-rate loans as a share of new originations have been steadily decreasing, reducing borrowers’ exposure to increases in market yields'; On the other hand, households were increasingly able to lock in historically low rates on long-term fixed-rate mortgages, creating a vast cushion of low-cost exposures that are not vulnerable to tighter monetary policies. Although both trends have briefly reversed in 2021, the overall picture remains positive when compared to the early 2000s. Additionally, households’ debt as a share of their gross income - which in the 2000s had gradually risen from 74% to 98% (to peak again at 96% in early 2021) - had declined to 84% in September 2024, signalling a greater ability to cope with loan-related payments11.

It should be noted, however, that significant differences remain in the usage of floating-rate loans across the euro area: fixed-rate mortgages remain uncommon in several Member States (including Estonia, Lithuania and Finland), and variable-rate loans continue to account for more than one fifth of new originations in roughly half of the euro area countries. The cost of new fixed-rate mortgages also shows significant cross-country segmentations, as shown in Figure 4. Lending rates in the Baltic countries are almost twice as much as in Malta and France; Baltic countries, together with Greece, are also those with the most expensive long-term, fixed-rate loans, making it more difficult for households to secure funding that is not vulnerable to future market rate increases.

Cross-country differences in rates do not, on average, mirror the credit spread paid by local governments (see the last two columns in the chart), but may be justified by a number of other factors (like loans issued to non-residents, the creditworthiness of borrowers, different lending standards in terms of, say, loan-to-value and loan-to-income ratios, the length and costs of the recovery process faced by banks on defaulted exposures). Such causes should be further investigated and, where possible, removed, to ensure that EU citizens benefit from a uniform and strongly integrated market for home loans.

Real estate risks and lending practices

The role played by banks’ origination practices and lending standards in the euro area can hardly be overstated. Loan-to-value (LTV) and loan-to-income (LTI) ratios at origination, as well as the original loan maturity, exert a statistically significant impact on loan default rates, meaning that loosening such parameters may lead to future losses and bank instability13.

Unsurprisingly, lending standards have been the focus of several recent supervisory exercises, involving both RRE and CRE. As concerns the former, (European Central Bank 2024) reports the results of a targeted review which examined 37 significant institutions with a combined loan portfolio covering 40% of all exposures held by all ECB-supervised banks. The study found significant differences across banks regarding:

- products, with some banks and jurisdictions engaging in loans insured but not backed by real estate collateral, loans with no formal mortgage but only a mandate to activate one in the event of credit deterioration, partially-amortising and interest-only mortgages with “bullet” capital repayment at the maturity date (sometimes accompanied by a savings account);

- origination criteria, with credit-granting policies often lacking important thresholds, such as LTV or debt-service-to-income (“DSTI”) ratios, or being based on “soft” limits subject to overrides;

- collateral valuation practices, with no valuations carried out by a professional appraiser (either external or internal) for roughly 40% of new RRE loans originated between 2021 and 2022, and 19 out of 37 institutions lacking energy performance certificates for more than 50% of newly issued loans.

Collateral valuation has also been addressed by recent supervisory analyses covering CRE loans (Darrieux et al. 2024), where assessments carried out by banks were reviewed by experienced appraisers, finding that the definition of “market value” was not homogeneous across institutions, with many banks assuming a “patient recovery” scenario that the ECB does not see as conservative enough14. Further shortcomings involved the use of outdated market data, the lack of transparency on the valuations’ underlying assumptions and the use of valuation methods that – while being acceptable in principle – were not adequate for the specific property that is being assessed. Additionally, banks were not promptly taking into account all factors (including, e.g., occupancy rates) that may drive down property values15.

The role of NBFIs: the case of real estate investment funds

Several NBFIs play an important role in financing the real estate market, including pension funds, insurance companies and real estate investment funds characterised as “alternative investment funds” (“AIFs”) under EU law. While all these categories of investors hold significant - and reciprocally entangled16 - exposures, this paragraph focuses on investment funds to present some detailed data on their assets and structure. This choice is motivated by the fact that pension funds and insurance companies typically use funds provided by long-term investors, and their customers’ ability to ask for cash advances is overall limited; this reduces the risk of liquidity squeezes and downward pressures on property prices. Additionally, as further discussed below, liquidity mismatches and the use of debt may make investment funds especially vulnerable to market downturns. Finally, as funds are heavily invested into by other financial institutions, contagion from real estate funds could significantly increase the banks’ overall exposure to property prices.

According to (Danieli 2024), real estate alternative investment funds in the EU have seen significant growth in the past five years (+375%, bringing assets under management, “AuMs”, to EUR 1.5 trillion). As of 2022, two thirds of AuMs were invested in physical, illiquid assets. On aggregate, real estate funds manage EUR 952 billion of real estate assets, that is, approximately 27% of the whole EU market, and invest predominantly in CRE (58% of net asset value, NAV, in 2022, down from 64% two years earlier17).

Although real estate funds must mark their assets to market, such valuations may occur less frequently than for liquid securities, meaning that they could become “stale” if property prices decline quickly. This may provide investors with an incentive to “rush for the exit”, redeeming their units as soon as they anticipate a price correction, before the latter is thoroughly reflected in the fund’s NAV. Indeed, recent supervisory reviews (European Securities and Markets Authority 2023) have found that the valuation models used by most real estate funds are based on a long-term perspective, prioritising stability over timeliness when asset values are updated.

According to (European Securities and Markets Authority 2024b), real estate funds suffer from a “liquidity mismatch”: e.g., while 19% of their liabilities (including units) has to be paid back within 90 days, only 4% of their assets can be liquidated within the same time horizon. At end 2022, only 16% of funds had in place a lock-up period for investors, while around 64% of open-ended funds (down from 70% in 2020) allowed redemptions subject to a minimum notice period; besides, 57% of real estate funds (in terms of NAV) were open-ended and 21% allowed for daily redemptions18.

80% of the funds’ NAV is held by institutional investors (that is, by well-informed players who may quickly rush for the exit in case of unfavourable developments), but these are mostly institutions that are relatively less subject to unexpected withdrawals, namely pension funds (accounting for 23%) and insurance companies (18%). Banks hold just 5% of the total NAV.

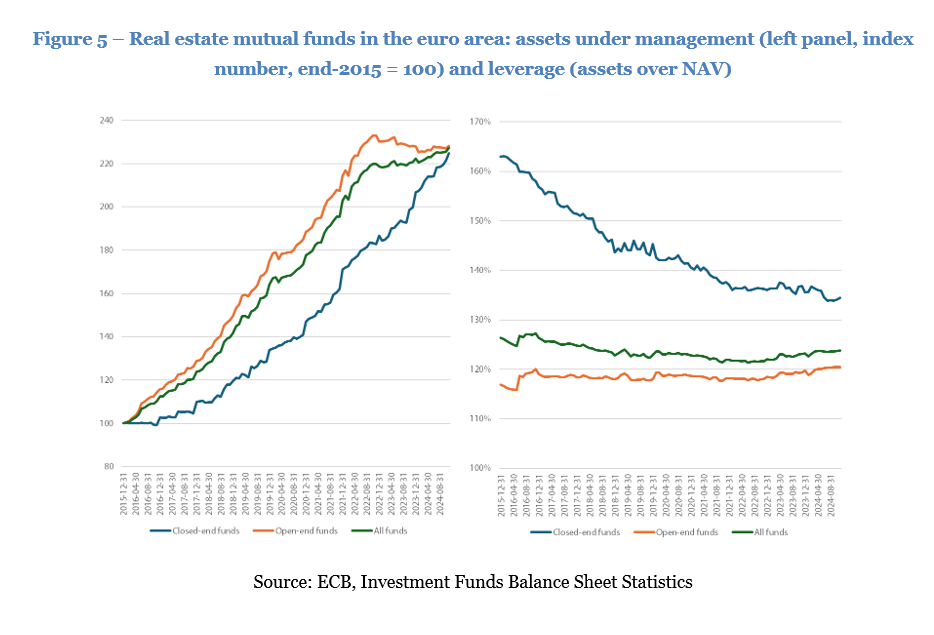

The use of debt by real estate funds represents another possible source of contagion, as part of the loans received could be withdrawn – creating liquidity imbalances and putting pressure on property prices – or remain unpaid, leading to losses for lenders. However, the funds’ average leverage (the ratio of total AuMs to NAV) remains overall acceptable (see Figure 5, right panel), and has indeed come down in the last decade, led by a significant decrease in the use of debt by closed-end funds. Figure 5 (left panel) also shows that the sector’s growth trend has slowed down and is mainly driven by closed-end funds, which are less prone to liquidity pressures.

Significant differences remain across Member States concerning the use of leverage (with Ireland close to 1.5 at end 2022, when new constraints on debt were introduced by the Central Bank19) and the role of open-ended funds (which represent 100% of the sector in France, and close to 90% in Germany). High leverage and a widespread presence of open-ended funds must be seen in conjunction with the large footprint that funds and other specialised investors exert in many national real estate markets.

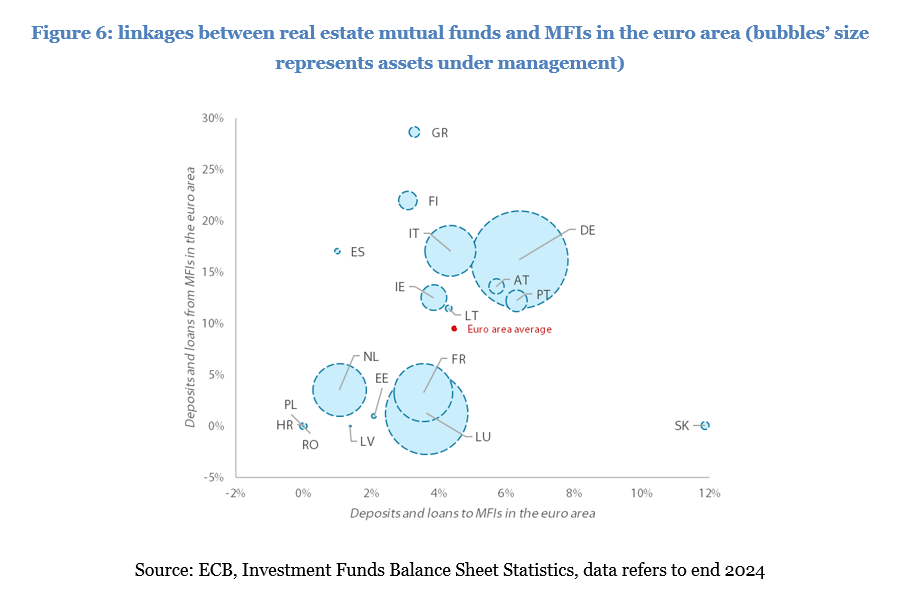

The link between real estate funds and the banking sector also looks very heterogeneous across the euro area, as shown in Figure 6. Although one should also look at the weight of long-term debt to appreciate each country’s vulnerabilities, the case of Germany is certainly eye-catching, also in light of the predominant role played by open-ended funds in that market.

Concluding remarks

This paper has investigated loans secured by real estate, reviewing some key market trends in terms of prices, credit risk indicators and the cost of mortgages.

The main policy implications of our analysis can be summarised as follows:

- too many national segmentations remain across Member States, and there is ample room for bringing national markets closer to the best practice: examples are the usage of floating-rate loans (which is still very high in some jurisdictions, leaving borrowers more vulnerable to interest rate spikes), the average cost of home loans, the (increasing) inability of low-wealth households to receive credit for house purchase purposes, the level of NPL ratios and their evolution over time. Such asymmetries should be further investigated, with a view to promoting a more efficient functioning of national markets;

- segmentations across Member States and individual banks also exist regarding lending standards. Not only are there differences in the levels of the main debt-sustainability indicators of newly originated loans (such as the LTV, LTI and loan-to-debt-service ratios), but such indicators are applied to heterogeneous products and rely on property evaluation practices that sometimes show significant scope for improvement;

- keeping the focus on banks should not prevent supervisors from closely following the evolution of NBFIs, which play a major role in real estate financing. An area of special interest are real estate funds, as the euro area is still a patchwork of national practices and rules, and efforts should continue to promote a level playing field and prevent the build-up of country-specific risks. Contagion channels to and from other institutional investors must be monitored through transparent and uniform reporting, as well as the banks’ involvement in financing real estate funds and investing in their activities;

- a holistic approach that addresses all funding channels supporting property investments without placing a disproportionate burden on traditional banks alone, looks as the most promising avenue towards enforcing a fair and effective supervision on real estate risks.

References

Danieli, Lorenzo. 2024. ‘Real Estate Markets – Risk Exposures in EU Securities Markets and Investment Funds’. Risk Analysis ESMA50-524821–3038. ESMA Reports on Trends, Risks and Vulnerabilities. Paris: European Securities and Markets Authority.

Darrieux, Sébastien, Christian Schmidt, Arnaud Saint-Sernin, Martin Mauger, and Chris Thorne. 2024. ‘Commercial Real Estate Valuations: Insights from on-Site Inspections’. Banking Supervision Newletter, no. August 2024 (August). https://www.bankingsupervision.europa.eu/press/supervisory-newsletters/newsletter/2024/html/ssm.nl240814.en.html.

European Central Bank. 2024. ‘Charting the Future: Risks and Lending Standards in Residential Realestate’. Banking Supervision Newletter, no. May 2024 (May). https://www.bankingsupervision.europa.eu/press/supervisory-newsletters/newsletter/2024/html/ssm.nl240515.en.html.

European Securities and Markets Authority. 2023. ‘Final Report on the 2022 CSA on Valuation’. ESMA34-45–1802. Paris: European Securities and Markets Authority.

———. 2024a. ‘Alternative Investment Funds (AIFs) Exposures to Commercial Real Estate’. ESMA50-1605533872–8484. Paris: European Securities and Markets Authority.

———. 2024b. ‘EU Alternative Investment Funds 2023’. ESMA Market Report ESMA50-524821–3095. Paris.

European Systemic Risk Board. 2023a. Issues Note on Policy Options to Address Risks in Corporate Debt and Real Estate Investment Funds from a Financial Stability Perspective. Frankfurt am Main: European Systemic Risk Board. https://data.europa.eu/doi/10.2849/24905.

———. 2023b. Vulnerabilities in the EEA Commercial Real Estate Sector: January 2023. Frankfurt am Main: European Systemic Risk Board. https://data.europa.eu/doi/10.2849/92721.

Gaudêncio, João, Agnieszka Mazany, and Claudia Schwarz. 2019. ‘The Impact of Lending Standards on Default Rates of Residential Real Estate Loans.’ 220. Occasional Papers. Frankfurt am Main: European Central Bank. https://data.europa.eu/doi/10.2866/04696.

Lang, Jan Hannes, Mara Pirovano, Marek Rusnák, and Claudia Schwarz. 2020. ‘Trends in Residential Real Estate Lending Standards and Implications for Financial Stability’. ECB Financial Stability Review 2020 (May): 107–21.

Lo Duca, Marco, Jan Hannes Lang, Barbara Jarmulska, Marek Rusnák, and Emil Bandoni. 2021. ‘Assessing the Strength of the Recent Residential Real Estate Expansion’. ECB Financial Stability Review 2021 (November): 38–40.

Resti, Andrea. 2025. Assessing Real Estate Risks and Vulnerabilities - Hidden Cracks in the Financial System? In-Depth Analysis, PE 764.379. Brussels: European Parliament. https://www.europarl.europa.eu/thinktank/en/document/ECTI_IDA(2025)764379.

Resti, Andrea, Marco Onado, Mario Quagliariello, and Philip Molyneux. 2021. ‘Shadow Banking: What Kind of Macroprudential Regulation Framework? - From Research to Policy Actions’. Study requested by the ECON committee PE 662.925. Brussels: European Parliament.

Ryan, Ellen, Barbara Jarmulska, Giorgia De Nora, Adele Fontana, Aoife Horan, Jan Hannes Lang, Marco Lo Duca, Claudiu Moldovan, and Marek Rusnák. 2023. ‘Real Estate Markets in an Environment of High Financing Costs’. ECB Financial Stability Review 2021 (November): 106–16.

Endnotes

1. This contribution is based on an in-depth analysis requested by the European Parliament (https://www.europarl.europa.eu/thinktank/en/document/ECTI_IDA(2025)764379), which benefited from insightful comments by Ronny Mazzocchi, Maja Sabol and Kai Gereon Spitzer (E-GOV). Comments on this version by Pedro Duarte Neves are gratefully acknowledged. All mistakes are mine.

2. As noted by (Lo Duca et al. 2021), rising prices and credit growth can be mutually reinforcing until a belated correction occurs. This correction can negatively affect household spending via wealth and/or confidence effects, leading to a drop in consumption. At the same time, losses on defaulted loans (including towards real estate developers) eat up capital and impair bank credit supply. The consequences can be exacerbated by the presence of numerous sources of indirect exposure, such as loans issued to large institutional landlords and to real estate mutual funds.

3. Real estate risks are explicitly mentioned in the ECB’s 2025-2027 supervisory priorities (see https://www.bankingsupervision.europa.eu/framework/priorities/html/ssm.supervisory_priorities202412~6f69ad032f.en.html).

4. See (Lang et al. 2020). According to the same authors, lending standards appear to be looser in countries that experienced stronger real estate expansions, suggesting that real estate vulnerabilities may have been growing in some euro area countries. For a review of previous research on the relationship between lending standards and default probability - as well as a multivariate empirical analysis - see (Gaudêncio, Mazany, and Schwarz 2019).

5. According to Lo Duca et al. (2021), the share of newly-originated loans with loan-to-value ratios above 90% was higher in 2020 than in the pre-GFC boom, while the share of loans with loan-to-income ratios above 6 - meaning households were borrowing more than six times their annual disposable income - was roughly equivalent to levels observed in 2007.

6. As noted by (Ryan et al. 2023), high financing costs reduce the affordability of, and demand for, real estate assets. An increase in interest rates also leads to a drop in the net present value of future rental income, which in turn affects the market value of real estate investments. This results in lower collateral values and higher loss rates on defaulted exposures. In the meantime, rising interest rates trigger higher debt service costs, increasing the probability of default. The fact that Loss Given Defaults (LGDs) rates and Probability of Default (PD) increase together may exacerbate systemic risk.

7. The uncertainty surrounding property prices has led (European Systemic Risk Board. 2023b) to recommend increased recourse to an array of possible micro- and macroprudential tools that are already being used by individual Member States (such as caps on the loan-to-value and the debt-service-to-income ratios, higher risk weights, and the use, when necessary, of countercyclical and systemic-risk buffers).

8. The use of home loans by individuals across the euro area is far from uniform, with some countries being characterized by levels that lie significantly above or below the region’s mean. Per capita debt is much higher in countries like Belgium and Ireland (about €27,000 and €26,000, respectively) than, say, in Hungary (approximately €2,000), Latvia (€3,000), Slovenia, Lithuania and Greece (€5,000).

9. Source: ECB Consolidated banking data.

10. The NPL ratio is the ratio of non-performing to total loans; the Stage 2 ratio is the ratio of Stage 2 loans (performing loans for which a significant increase in risk has occurred since origination) to total loans subject to impairment review.

12. 2025 data refers to the first four months and was weighted accordingly. Data for Croatia refers to 2023-2025.

13. Based on loan-level data for residential loans in eight euro area countries, (Gaudêncio, Mazany, and Schwarz 2019) have shown that a 10 percentage points increase in LTV at origination raises the average probability of default (PD) by 0.2. Similarly, an increase in the borrower’s LTI ratio by 1, or extending the original maturity by one year, elevates the average PD by 0.1%. These are material impacts, given the sheer size of mortgages in many EU countries and the fact that defaults tend to happen in waves.

14. A contribution towards more homogeneous and conservative valuations could come from CRR3 (effective from 2025), according to which the value assigned to collateral must exclude expectations of price increases and must be adjusted for the risk that current market values be above the “long term”, sustainable value of the asset.

15. It is unclear, however, whether the advantages of adopting proactive valuation methods would offset the risks triggered by an approach that may prove overly procyclical by increasing expected losses, curbing the lenders’ willingness to support further real estate transactions and putting further pressure on the market (ultimately turning into a self-fulfilling prophecy).

16. Pension funds and insurance companies are among the main participants in real estate funds; as reported in (European Systemic Risk Board. 2023b), e.g., more than a third of EU insurers’ investments in CRE at end 2021 took place indirectly, via investment funds.

17. According to (European Securities and Markets Authority 2024a), there are 2,675 real estate funds marketed and/or managed by authorized EU alternative investment fund managers, with a total NAV of €607 billion. Within this sample, 2,131 funds were pursuing a CRE strategy “primarily”, while another 544 pursuing it only “partially”.

18. Against this backdrop, the review of the Alternative Investment Fund Managers Directive (Directive 2011/61/EU, “AIFMD”) has introduced an obligation for fund managers to adopt at least two “liquidity management tools” aimed at reducing the “first mover’s advantage” and preventing sudden waves of redemptions. Such tools include redemption gates, extended notice periods, redemptions in kind and anti-dilution tools like redemption fees, swing pricing, dual pricing, anti-dilution levies (Resti et al. 2021).

19.See (European Systemic Risk Board. 2023a).

Andrea C. Resti is a professor of banking and finance at Bocconi university, Milan, where he teaches financial risk management. He took part in the first European Banking Authority’s Stakeholder Group, where he served as vice-chair and coordinated the Group’s activities on bank liquidity rules. Since 2016 he serves as an advisor on banking supervision to the European Parliament. He has acted as a consultant to a large number of banks, rating agencies and supranational institutions, and as an expert witness in financial misconduct cases. He has been a board member at various financial institutions. He has published international books and articles in top academic journals, as well as many ad hoc reports requested by the European Parliament and more than 500 columns in financial newspapers and websites.